Are Foreigners Dumping US Treasuries?

Are Foreigners Dumping US Treasuries?

Issue 91

✌️ Welcome to the latest issue of The Informationist, the newsletter that makes you smarter in just a few minutes each week.

🙌 The Informationist takes one current event or complicated concept and simplifies it for you in bullet points and easy to understand text.

🫶 If this email was forwarded to you, then you have awesome friends, click below to join!

👉 And you can always check out the archives to read more of The Informationist.

Today's Bullets:

An Auction Scare

Some Details

The Big Picture

The Worry

Inspirational Tweet:

We've been hearing quite a bit of concern about demand for US Treasuries lately, especially from foreign buyers.

Are foreign central banks and foreign holders of USTs now net sellers of the global reserve asset? A pretty frightening thought if you're the US Treasury.

Or, as TXMC points out above, is this concern completely overstated and overblown? (BTW, if you are not yet following TXMC on Twitter/X, you should, his analyses are fantastic and always insightful).

In any case, there's plenty of confusion and perhaps data obfuscation in this ongoing debate, one that deserves a closer look. And that's exactly what we are going to dig into here today. But have no fear, we will do it nice and easy, as always.

So, grab that cup of coffee, saddle up and settle in for a short loop around the US Treasury market with The Informationist.

😱 An Auction Scare

Much of the recent concern over demand for US Treasuries has been exacerbated by a recent bond auction.

The 30-year US Treasury debacle.

If you've been following along with The Informationist and have been reading my posts and threads on Twitter/X, you are well aware that the latest 30-year bond auction was absolutely abysmal.

Downright scary, in fact.

For those who have not been following and are now asking, why?

The answer is: because demand fell off a cliff, especially from foreign buyers.

How far (or how fast) off a cliff?

Not quite Wile E. Coyote style, but...

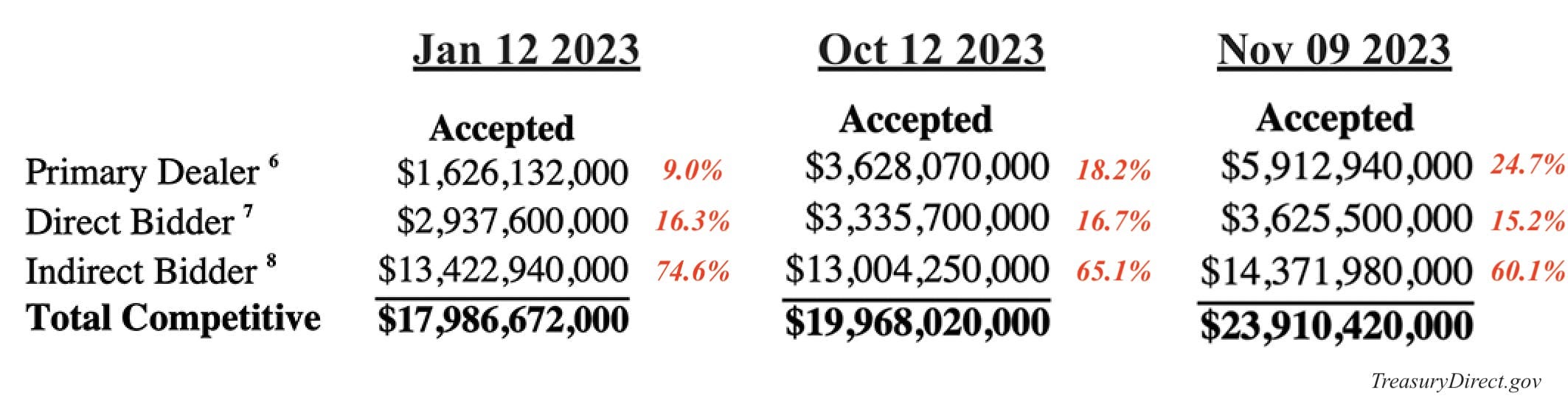

Here's a graphic many of you have seen, let's revisit and focus in on the Indirect Buyers, who are the foreign buyers of each of these 30-year Treasury auctions that occurred over the course of this year:

Yes, you are reading that correctly, foreign demand as a percentage of the total has dropped by ~15% over the last 10 months.

So, maybe we're more like here in the fast evolving Treasury tragic comedy.👇

Question is, why was this auction in particular so poor? Are buyers suddenly fleeing en masse? Or was it just a blip in the process, and nothing to see here, move along, kind of event?

I can think of a few explanations and possible reasons for the poor auction, and we'll get to those in a bit.

First, let's turn to some facts and figures. See what the actual data is really telling us.

We'll take the temperature of Treasury demand, so to speak. Then we'll dig deeper by way of zooming out a bit.

🧐 Some Details

Let's face it, when we see a chart like this, it appears obvious that China, the second largest holder of US Treasuries, has been aggressively selling them out of their reserves.

Problem is, this chart is a bit misleading, as it suggests that China has been reducing their holdings, and this selling has picked up significantly in the last year.

The reality is, this chart (and many others like it) are showing the total market value of holdings, and how that has been changing from month to month, year to year.

As you recall, the US Fed had been raising rates at a rocket pace during that time, taking not just the Fed Funds yield up, but every single yield of the various US Treasuries along with it.

You see where I'm going with this.

Exactly. Rising yields means falling prices for bonds.

And so, as bond yields rose across the spectrum, all those prices fell, leading to the worst rout in bond market history, destroying trillions of dollars in mark-to-market holdings of US Treasuries, depleting bank reserves, causing regional bank failures (a la Silicon Valley Bank), and all but obliterating the 60/40 equity/bond portfolio along the way.

Add to this, the confusion of the way the US Treasury has reported foreign holders of USTs, convoluted, obfuscated, and downright lazy, and misinterpretations and incorrect assumptions have flourished.

Why?

Because the Treasury International Capital (TIC) reported holdings as: "Aggregate Holdings, Purchases and Sales, and Fair Value Changes of Long-Term Securities by U.S. and Foreign Residents."

In other words, the TIC commingled the mark-to-market with purchases and sales to come to their reported numbers.

This made it virtually impossible for analysts to determine the actual purchases and sales from month to month. And has yielded charts like this one:

Problem is, this chart is using data from the Council on Foreign Relations and likely estimatingmark-to-market and extrapolating total net purchases and sales through data from large investment banks and custodians.

There was really no better way to do it, as far as I can tell.

This however, has recently changed,

Because new data at the TIC seems to break the actual purchases and sales out by country and by month, separately, for us to take a closer and more accurate read as to what is going on with underlying demand for US Treasuries.

The reality is still not fantastic, but it is a little different than I would have expected.

For instance, when looking at China, we can see that the actual purchases and sales reported by the US Treasury (in its new breakouts) differ wildly from the charts above.

In fact, China, its central bank and its investors, have been net buyers of USTs this past eight months (since the new TIC reporting began). Which makes one wonder just how badly those investors were leaning on the long end of the curve, leading to all those mark-to-market losses we see above.

As far as global foreign demand for US Treasuries, the picture is disturbing at best.

Yes, you are seeing that correctly. Though it seems to have picked back up in September, it looks like foreign holders of US Treasuries have, in fact, been net sellers of ~$300B worth of USTs this year. So, then, it is no surprise that we had such a dismal 30-year bond auction a few weeks ago.

This is not great news, considering the amount of USTs the Treasury has been issuing this year.

Let's zoom out a bit to determine if the net selling of foreigners parallels with the overall holdings of outstanding Treasuries.

😮 The Big Picture

If we look at foreign holdings of US Treasuries as a percentage of total outstanding, we can, of course, see if there has been a decrease in foreign demand.

After all, everyone is mark-to-market in this measure, so that largely removes the price variability of foreign holdings vs. domestic. This cuts out a little of the market price noise.

And yep, foreign holdings have been decreasing steadily over the last decade, sitting at about 23% of total outstanding debt at the beginning of 2023.

Drilling in a bit tighter, we see that foreign holdings as a percentage of total marketable debt outstanding. This is basically a measure of the foreign holdings of actual public market of debt, which would exclude inter-governmental and private transactions by the Treasury.

An even better measure of demand, IMO.

And still pretty ugly, having been steadily decreasing and hitting 30% at the beginning of 2023.

This is down from ~50% of foreign holders 10 years ago .

Warning sign, indeed, and dovetails with the data we are getting for this year.

But foreigners haven't been selling that many Treasuries. What gives?

Well, many holders of USTs are clearly letting ones that they already own just mature off their books and they're not replacing them.

And then, of course, there's the insatiable appetite of the US Treasury, the entity that must find a way to finance all the reckless spending coming out of DC.

And how do they do that?

You got it.

They issue massive amounts of USTs, financing government deficits with more and more and more...

Debt.

😰 The Worry

Truth is, we've piled on $2.4T of federal debt in 2023, thus far.

Considering we are doubling the amount of debt every ~10 years or so, we're going to need to issue an additional $17T in just the next five years.

And with a likely coming recession and growing federal deficits, this could be more. Much much more.

Makes sense that foreign investors wary of buying USTs, participating at a lower rate and actually becoming net sellers this past year, doesn't it?

A few reasons for wariness:

A persistently strong USD makes it more expensive for foreigners to buy USTs and entices holders to sell their USTs to get USDs in order to get more of their local currency

Concern that the Reverse Repo Facility will soon run dry, forcing the Treasury to issue far more long duration bonds, which will weigh on the prices of them (and cause losses for buyers)

Worry that US inflation will persist, making the Fed keep rates high, and diminishing the value of longer duration bonds, such as the 30 year UST

Concern that the US government is running such high deficits that the Treasury will have no choice but to flood the markets with bonds soon, and the Bond Vigilantes will demand 'term premium' as compensation for this risk (also causing losses for buyers)

Incidentally, I've written all about the Reverse Repo dynamics related to Treasuries as well as Bond Vigilantes, and if you have not yet seen those you can find them and other recent articles right here,

Bottom line, foreign demand for US Treasuries is declining at the exact same time the Treasury needs more buyers.

More demand.

If they've broken out and are reporting the data correctly now, there is plenty of cause for worry.

I believe we will see plenty of clues in upcoming auctions, ones that will give us insight into the underlying demand, especially from the foreign (or Indirect) bidders.

The worry, of course, is that the Treasury just overwhelms the market with too many bonds, and the demand just isn't there for them. If that happens, the Fed and Treasury will need to step in to ensure sufficient liquidity in the Treasury market.

This is the one market in the world that cannot lock up. It must remain orderly and have sufficient liquidity at all times.

You better believe I'll be watching what goes on in these auctions and adjusting my allocations accordingly.

I strongly suggest you do, too.

And if you have not seen my breakdown on how to read Treasury auctions, you can find it right here, explained super simply, as always:

That’s it. I hope you feel a little bit smarter knowing about US Treasury foreign demand and their implications for the overall markets.

If you enjoyed this newsletter and found it helpful, please share it with someone who you think will love it, too!

Talk soon,

James✌️