The Bank of Japan Experiment

✌️ Welcome to the latest issue of The Informationist, the newsletter that makes you smarter in just a few minutes each week.

🙌 The Informationist takes one current event or complicated concept and simplifies it for you in bullet points and easy to understand text.

🧠 Sound smart? Feed your brain with weekly issues sent directly to your inbox:

Today's Bullets:

Abenomics

BoJ and Yield Curve Control

Implication for Treasuries

Can the US become Japan?

Inspirational Tweet:

You've likely heard about the Bank of Japan (BoJ) and the yen lately, and how they are an important factor in macro-economics these days.

But what is the BoJ doing that is so important, and could what is going on all the way out there impact the US markets?

The short answer: yes, and it is.

The long answer: well, we're going to have to unpack this piece by piece for it to make sense. But don't worry, we will tackle it nice and easy, as always, today.

So, grab that cup of coffee and settle in for a Sunday session with The Informationist.

🤑 Abenomics

First, the Japanese yen (JPY) used to be a flight to safety currency. Super strong.

Lately, though, it has been anything but a flight to safety and has been rather weak. Super weak.

In fact, you can get almost 150 yen per USD these days, a level we haven't seen since the late 1990's.

So, what happened to the yen?

Abenomics happened. When this whole Japanese central bank experience began.

It all started for Japan back in the late 1980s, when, after an extended and relentless expansion in the real estate market, the BoJ started aggressively raising interest rates.

Can you guess what followed?

You got it. The speculative real estate bubble burst and plunged the economy into a severe downturn.

It was like tsunami of disinflation, and it caused what has been dubbed as The Lost Decade of Japan that lasted from 1991 to 2001.

And as if their overly stimulating and then overly restrictive policies (read: manipulations) were not enough, the BoJ then doubles and triples down through an experiment known as Abenomics.

Abenomics refers to economic policies put in place by Shinzō Abe, during his second term as the Prime Minister of Japan from 2012 to 2020.

But unlike what has been going on with inflation in the western world for the last few years, the primary objective of Abenomics was to overcome deflation and to rejuvenate a stagnant Japanese economy.

The plan had three core components, known as the three arrows of Abenomics:

Monetary Easing: Aggressive monetary policy aimed at achieving a 2% inflation target

Fiscal Stimulus: Short-term fiscal stimulus through government spending

Structural Reforms: Long-term strategies to boost Japan's economic growth, such as labor market reforms, corporate governance reforms, and initiatives to boost competitiveness

So, in December of 2012, when Shinzō Abe returned as Prime Minister, he immediately advocated for aggressive monetary easing to combat deflation and stimulate growth.

What followed in early 2013, was the Bank of Japan (BoJ) adopting a 2% inflation target and then an intense phase of quantitative easing (QE) to double the monetary base in two years.

Along the way, the government then increases consumption taxes, but the economy responds negatively (imagine that 🙄) and they postpone any further increases.

Instead, by 2015, BoJ introduces a negative interest rate policy.

Not enough, Abe announces a ¥28 trillion stimulus package to rejuvenate the economy. This equated to ~$233 billion, a lot of money back in 2015.

The BoJ remained committed to its 2% inflation target and maintained its ultra-loose monetary policy all the way through Abe's retirement in 2020, and up to today.

The result?

The moves initially spurred stock market growth and weakened the yen, which benefited exporters, and made some progress in combating deflation.

But it was still not enough.

The BoJ then doubled and tripled down on manipulation this past couple of years, instituting what we call yield curve control.

🤨 BoJ and Yield Curve Control

Put simply, yield curve control is when a central bank enters the open market and buys and sells bonds of specific maturities in order to keep interest rates at a certain level.

Remember, central banks set what is called the target rate, but this is an overnight rate. The remaining maturities of bonds, i.e., 1 mo, 1 yr, 2 yr, 10 yr, etc., are priced off of this target rate, according to the length until they mature, among other factors.

What I mean is, all other bonds are priced by the market, according to market risks and factors.

Unless of course the central bank enters that market and manipulates it to get the bonds to trade at yields that they want them to.

Yield curve control.

This move is significant in and of itself. However the direction that the BoJ has been moving rates is even more significant.

See, in 2021, when virtually all the other central banks from developed countries were raisingrates to combat inflation, the BoJ was manipulating their rates lower.

In fact, they kept their benchmark overnight rate negative and then put a target on their own 10yr JGB (Japanese treasury) of just .25%.

Here's the problem.

As I noted above, interest rates around the world were rising.

Japanese investors noticed this and, starved for yield locally, they began searching for yield elsewhere.

When this happens, the low yielding country's currency suffers.

This relationship of currency and yields is called interest rate parity.

And why not? If they could get over 4% return on a US Treasury, why would they remain invested in a bond that returns .25%?

Problem is, to do this a Japanese investor must sell his JGB and then sell the yen he gets for it to buy USD in order to buy the USTs.

Sell JGB Treasury → Receive yen → Sell yen and buy USD → use USD to buy USTs

So, basically, with yields being held artificially low, pressure builds up in the Japanese markets and that pressure has to be released somewhere.

The escape valve is effectively the yen, and it has suffered due to interest rate parity.

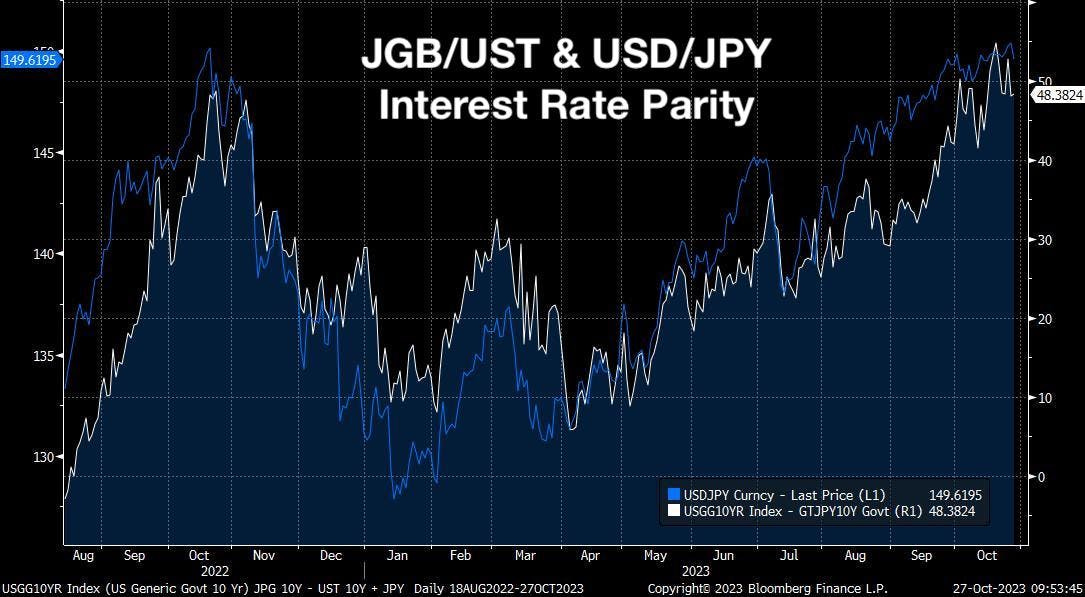

Here is a chart showing the relationship between the difference between the 10yr JGB yield and the UST yield and the USD/JPY crossrate:

You can see how the price of the yen is directly related to the difference in yields of the two government bonds.

As the difference in the yields rises (the more yield you can get by buying USTs instead of JGBs), the currency weakens (the more yen you get per USD).

The Fed started raising rates, the BoJ manipulated theirs' lower, the yen has suffered.

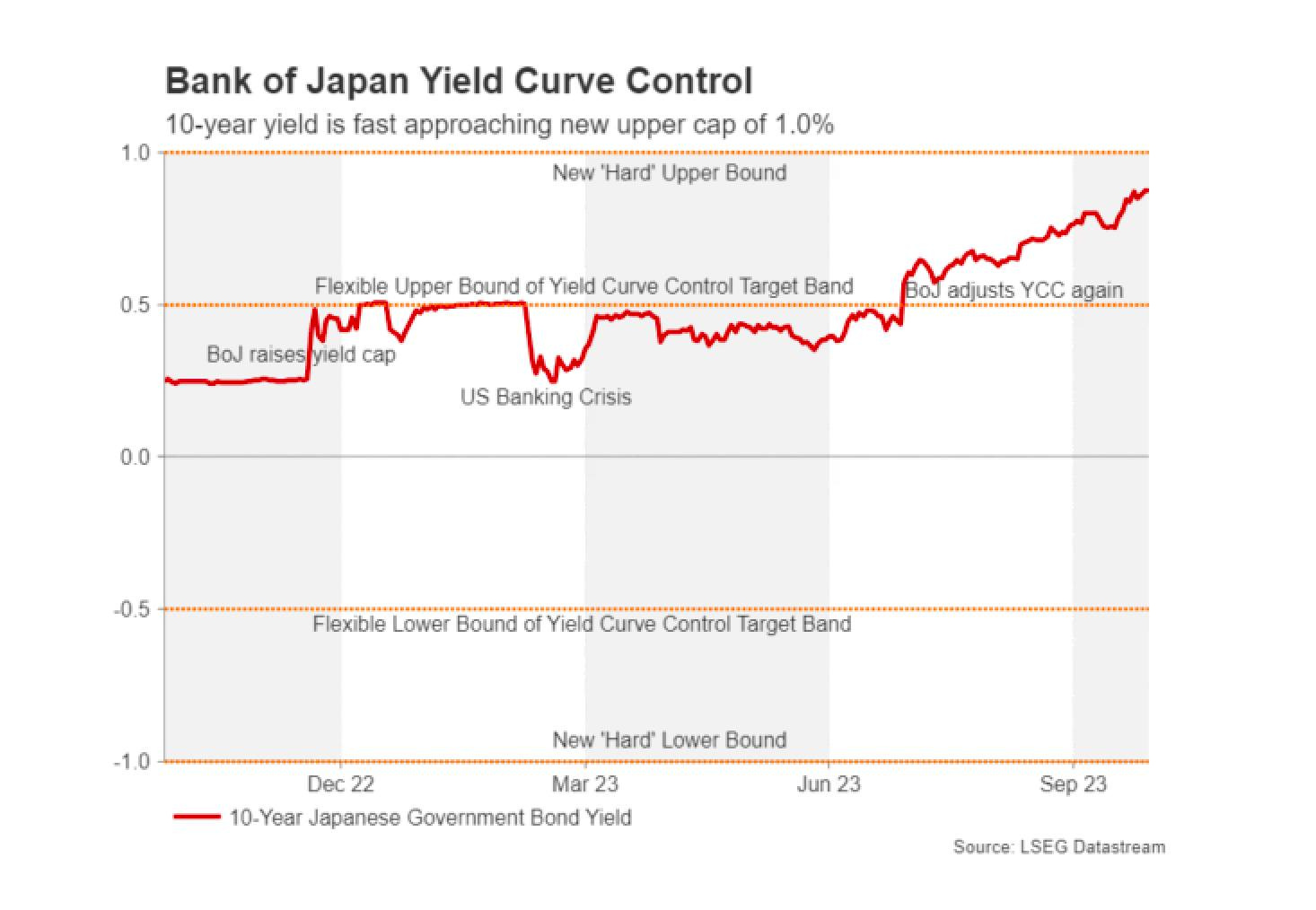

In February, this pressure got to be too much for the yen, and so the BoJ moved the 10yr target rate up from .25% to .5%.

The result was a short-lived reprieve for the yen.

But it was only momentary, as the Fed continued to raise rates, putting pressure on the JGBs once again.

The yen continued to weaken until the BoJ capitulated in July, moving the absolute top of the JGB 10yr yield range up to 1%.

But the pressure remains, as the yen continues to weaken toward 150, forcing the BoJ to repeatedly execute what they call extraordinary measures to support their currency along the way.

😨 Implication for Treasuries

Though they are hardly extraordinary, as the BoJ has been executing the, semi-regularly for years now, buying yen, buying JGBs, changing targets, changing upper and lower bounds of targets...what a mess.

Here's the issue, though, and back to the original question inspired by today's Tweet above: what does this have to do with the US and its markets?

The US has its own problems with a growing deficit, a mountain of (also growing) debt, and worries from investors who are pushing the yield of that debt higher to be compensated for long-term inflation risks.

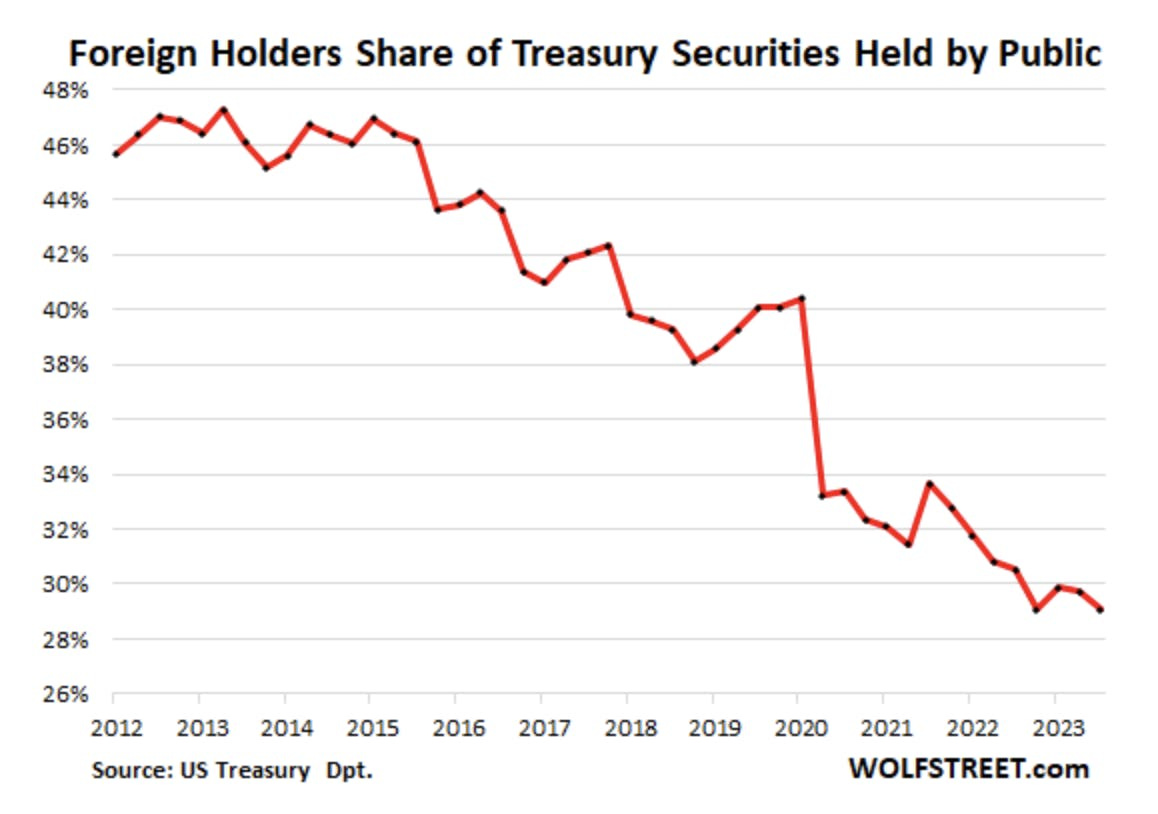

This is on top of (or perhaps adding to) the US Treasury losing luster around the world.

International investors are either not adding to or decreasing their holdings of USTs the last number of years:

And now, as the yen remains under pressure from artificially low rates in Japan, with investors selling their JGBs and buying higher yielding debt elsewhere in the world, how is the BoJ responding?

You got it, they are either allowing the USTs they hold at the BoJ to mature off their books or outright selling them and using the USDs to buy and stabilize the yen.

And until the BoJ fully relents and allows JGBs to trade at truly market driven prices, this will only get worse, adding significantly to the pressure on the US 10yr UST.

Why?

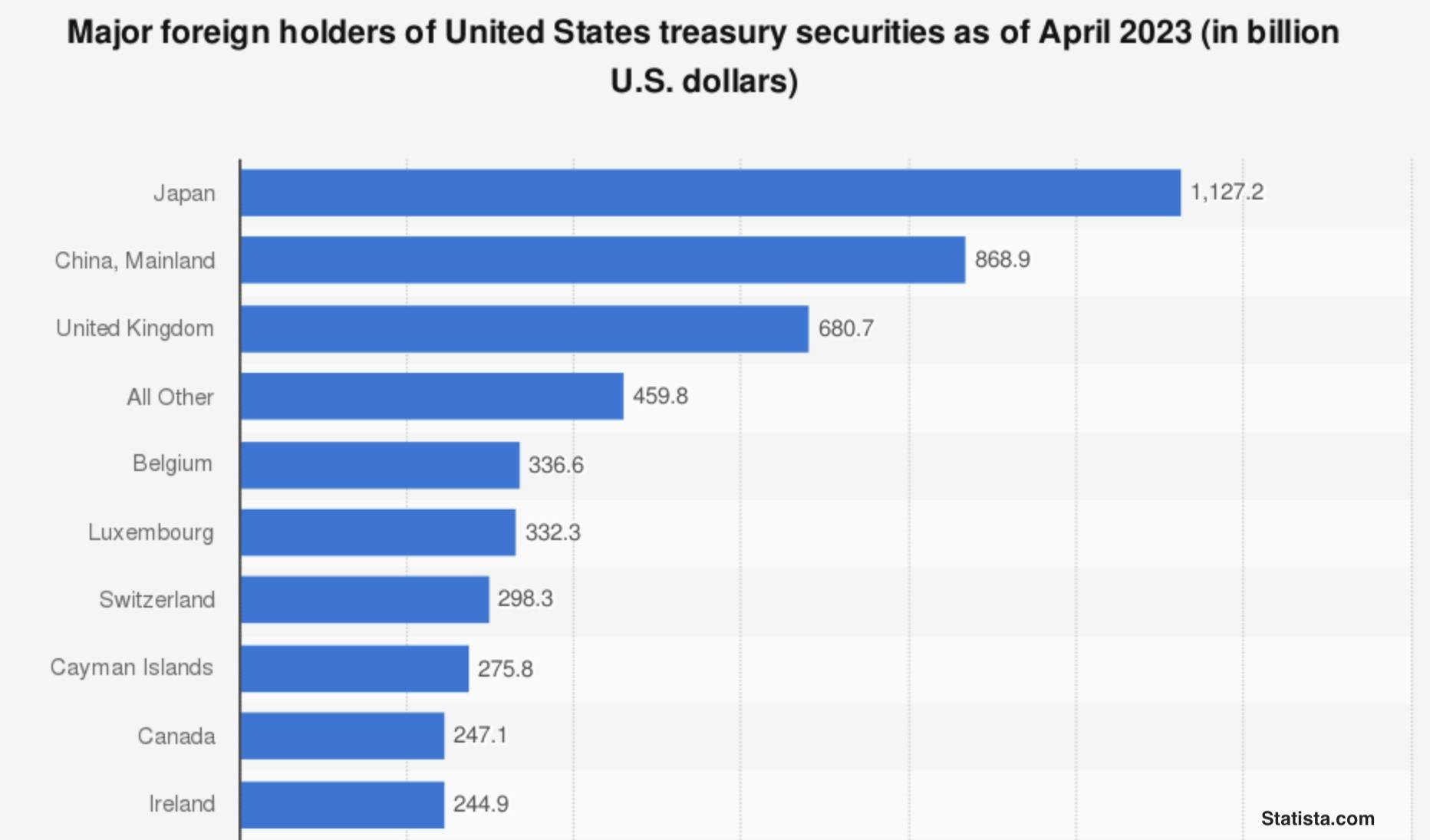

Guess who is the largest owner of USTs outside the US?

You got it. Japan.

Unless the BoJ gets comfortable with the yen topping 150 and remaining there, the pressure on USTs will continue.

So, buckle in and keep your eye on the BoJ and its policies over the coming months. I know I will.

But, I also won't be surprised if we start hearing about swap lines being opened between the Fed and the BoJ, to ease their USD/JPY woes.

If you're wondering what I mean by that, I wrote all about it in a recent newsletter, you can check it out here:

TL;DR: The US will loan USD to anyone and everyone to be sure the US Treasury market remains highly liquid and stable at all times.

🥸 Can the US become Japan?

One last thing.

I get this question all the time, so let's address it really quickly.

Can the US do the same thing as Japan? Just keep printing money, keep buying its own debt, keep rates where they want them, and allow debt to GDP balloon to (even more) obscene levels?

The answer is yes and no.

Yes, because the US has a distinct advantage over Japan in that the US is fortunate to have both the global reserve currency and, by extension, the global reserve asset in the USD and the UST.

This gives the US Treasury and Fed a tremendous amount of rope to work with and leeway to manipulate around their own bonds and currency.

Because even though foreign holdings is falling, there is still a massive amount of demand for USTs and USDs around the world.

But still, this only gives the US rope and time. Because the two countries have entirely different structures and demographics.

Japan has an aging demographic, has already had their real estate asset bubble burst, and they are net exporters.

The US, on the other hand, has a bubbling real estate market and is running twin deficits, being a net importer.

In my opinion, the US cannot imitate Japan, although it sure looks like they are going to attempt it. I expect plenty of yield curve manipulation and control to keep rates from going too high. I also expect plenty of debt monetization, especially in a market event that threatens UST liquidity.

And this can go on for a long time.

A long long time. Like decades.

But one other thing I am highly confident of: it cannot go on forever.

At some point, the world wakes up to the relentless and unabashed debasement of the USD and the UST, making them worth less and less, until they are virtually worthless.

So position your portfolios for long long term stability with hard currencies, and plan accordingly.

That’s it. I hope you feel a little bit smarter knowing about Japan and Abenomics, and are ready to start incorporating some of this knowledge into your own investing process.

If you enjoyed this newsletter and found it helpful, please share it with someone who you think will love it, too!

Talk soon,

James✌️