The Implications of the Basis Trade

The Implications of the Basis Trade

Issue 95

✌️ Welcome to the latest issue of The Informationist, the newsletter that makes you smarter in just a few minutes each week.

🙌 The Informationist takes one current event or complicated concept and simplifies it for you in bullet points and easy to understand text.

🫶 If this email was forwarded to you, then you have awesome friends, click below to join!

👉 And you can always check out the archives to read more of The Informationist.

Today's Bullets:

What is the Basis Trade?

How big (of a problem) is it, really?

Long Term Memories

Inspirational Tweet:

The hedge Fund 'Basis Trade', something you may have been hearing about lately and may hear much more about in the coming year.

Yes, yes, I keep hearing the term 'basis trade', but what the heck is it?

Look, this basis trade business can get really complicated, really fast. But we're not going to go down that path.

One, because we don't do that here at The Informationist.

And two, there really is no need to get super complicated in order to understand the essence.

The simple market risk imposed by these massive positions.

But how are big are the risks, what's the real danger, and could it impact your portfolio?

Great questions, and ones we will answer, nice and easy as always, here today.

So, grab your favorite cup of coffee, saddle up, and settle in for a quick trot down the hedge fund bond path today with The Informationist.

🤓 What is the Basis Trade?

Put simply, the Basis Trade, as it has come to be known, is an arbitrage trade between two similar securities.

You know, buying one security and selling short another very similar one, capturing the spread in-between. That kind of arbitrage.

In this case, the trade is buying a US Treasury (cash settled) and selling a US Treasury (future settled) against it.

Traders do this when the two securities are mis-priced relative to each other, anticipating the mis-pricing will correct itself. The idea is to gain on one side of the trade enough to offset any loss on the other side, resulting in a net profit.

When doing this in the futures market, basis trading becomes profitable if the purchase price plus the net cost of carry is less than the futures price.

And 'basis' refers to the difference between the spot price of the cash market bond and the price of its related futures contract.

Problem is, this difference and the net profit from the cost of carry spread is so minuscule that traders must use leverage to make it worth their while.

Mountains and mountains of leverage.

But let's put that aside, we will get to that next.

First, let's just lay out a simple example to understand the trade.

Scenario:

10-Year Treasury Bond in Spot Market: Let's say it's trading at $98.00

10-Year Treasury Bond Futures Market: The corresponding futures contract is trading at $99.00

Basis Trade Setup:

The Basis: There's a price difference between the spot market and the futures market. The futures are trading higher than the spot price. The difference of $1.00 ($99.00 - $98.00) represents the basis

Executing the Trade:

Buy in Spot Market: You buy the 10-year Treasury note in the spot market at $98.00, anticipating a rise in its price or a decrease in the basis

Short Sell Futures Contract: Simultaneously, you sell short a 10-year Treasury futures contract at $99.00, expecting the futures price to fall or the basis to narrow

The Expectation:

Your aim is for the basis between the spot and futures market to converge. This can happen if the spot price rises, the futures price falls, or both.

Outcome Scenarios:

Basis Converges (Profit): Over time, suppose the spot price of the Treasury note increases to $98.50, and the futures price decreases to $98.50. The basis has converged to zero. You sell the Treasury note in the spot market and buy back the futures contract. Your profit is $0.50 per Treasury note from the spot market and $0.50 per contract from the futures market, totaling $1.00 per combined position.

Basis Widens (Loss): If the basis widens (i.e., the spot price decreases to $97.50 while the futures price remains at $99.00 or rises), this would cause a loss on your position of $1.50.

Reality:

The basis or spread in real world basis trades are much much tighter (smaller). We are talking mere basis points or hundredths of a percent per trade, not half a percent or more.

Also, there is a loan cost associated with the trade, borrowing fees as well as trading fees, which can add up to eat into the basis of the trade.

And so, as we noted above, traders will often use large (read: massive) amounts of leverage to make it worth their while.

They can do this because they are executing this trade simultaneously and at scale.

In other words, the hedge fund goes long the basis trade by simultaneously purchasing Treasuries (using repo loans facilitated by its Prime Broker) and shorting a futures contract of a similar Treasury.

The ultimate profit on the trade is the difference between the price of the cash Treasury and the futures Treasury minus the interest cost on the repo loan and any trading costs.

This whittles the arbitrage down to mere basis points, requiring leverage to make it profitable enough in terms of actual dollars.

But how much leverage are we talking about, and how big of a problem could it be?

🫣 How big (of a problem) is it, really?

First things first.

We know the traders who are doing basis trades are not traditional long-only money managers. By definition, they must be able to short against their positions. So, who are they?

You got it. Hedge funds.

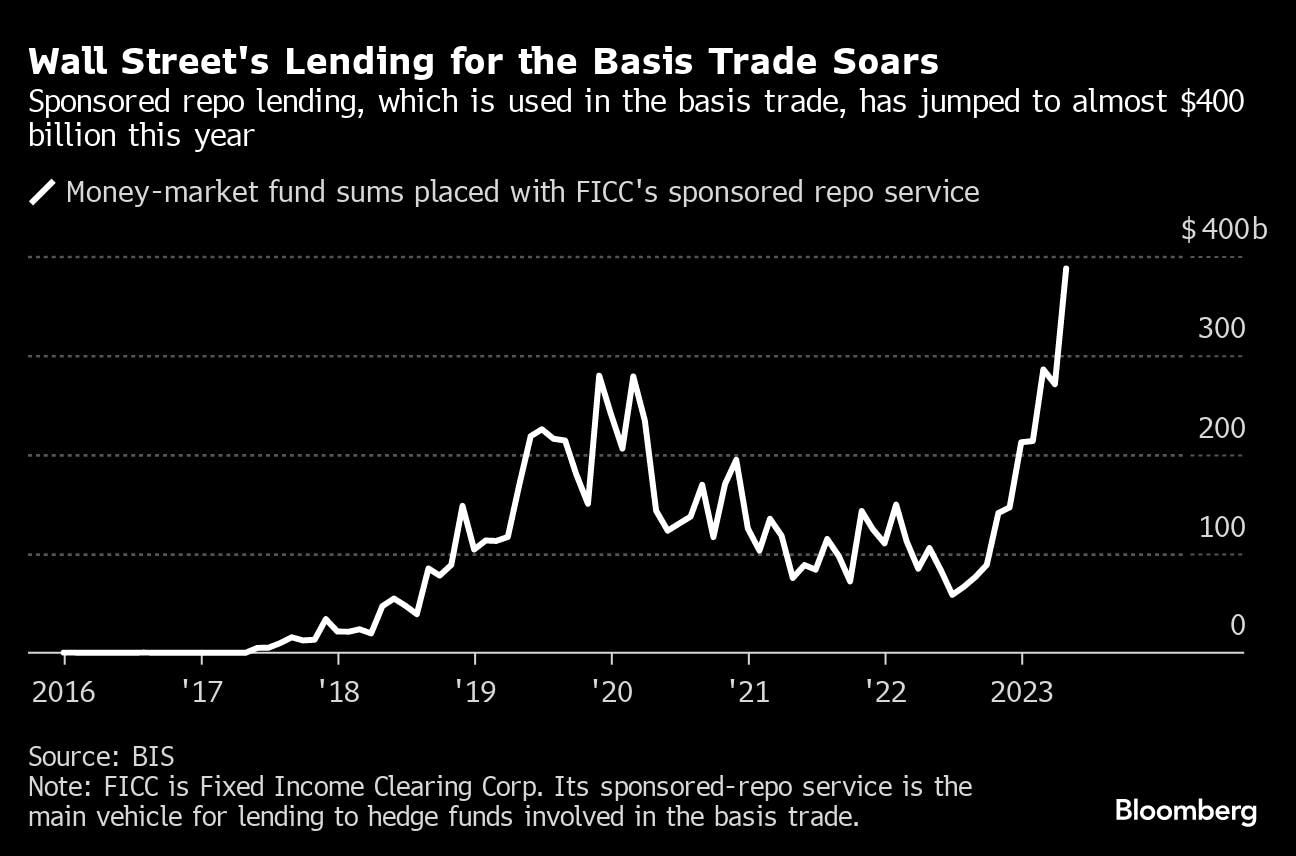

And if we look through to the repo lending facilities (the non-Fed private repo market), we can see how much they have been borrowing to facilitate these trades.

Mind you, this is not the only source of borrowing, but it gives us an idea how much the trade has grown this year.

Quite a bit, it seems.

And there are widespread reports that these basis trades are on leverage of over 50 to 1.

Yikes.

Put a pin in that, we will come back to leverage in the next section.

But first, you may be thinking: OK, hedge funds are buying cash Treasuries, but it's obvious that there are plenty of those on the market. Just look at the avalanche of debt the Treasury has been auctioning off lately, and it's no surprise that off-the-run (older issues) would be trading at attractive prices for hedge funds to scoop up in the basis trade.

But hedge funds are also shorting the futures, so who is buying all of those futures contracts and why?

Taking a peek at data from the CFTC, we get our answer.

Simple long-only asset managers have been buying the futures contracts from the hedge funds who are shorting them.

Why?

Well, there can be a few reasons for this, but one of the main ones is that futures contracts require much less capital to execute, as you are not buying the cash value, but rather a contract (a derivative) on that cash value.

So, a long-only money manager, like a pension fund or endowment, can access a simple kind of leverage here, multiplying the returns he would get on a bet, for instance, that interest rates will be lower by the time that contract expires.

And on the other side of that bet, the hedge fund manager is playing the basis trade, just hoping that the difference between the future and the cash Treasury will converge.

Ah, the wonder of efficient capital markets.

And how much are we talking about in total dollars? What kind of exposure do these hedge funds have to the so-called basis trade?

Would you believe over a trillion dollars just last month?

Well then.

No wonder Gensler's shorts are all tied up in knots (pun intended), and he's introduced new rules for 2025 that would require more oversight of these private repo transactions.

But, it is important to note that these trades have already started to be unwound.

It has been reported by Reuters that funds have cut their gross short position in two-year futures three weeks in a row, and it looks like the record short of 2.65 million contracts in the week to Nov. 7 will prove to be the peak.

And the record short aggregate position of over $1 trillion across two, five and 10-year futures (seen in the blue line of the above chart) has been cut to about $970 billion.

OK, then.

The risk is easing. The basis trade is fading. All is well and the risk is gone, right?

Happy Holidays, crack open the champagne, and get that prime rib in the oven already.

Right?

Hold on. Hold on. Hold on.

There is one teeny little problem that remains, in my opinion.

The sheer concentration of these trades is staggering.

In fact, almost 50% of all basis trades are held but just eight (or fewer) traders.

Call me an alarmist, if you will, but a trillion dollars of massively leveraged exposure on eight books (or fewer) is cause for at least a pause.

I mean, doesn't anyone remember Long Term Capital Management for God's sake?

🤯 Long Term Memories

I won't get into the entire debacle from the 1998 crisis caused by LTCM arrogance and hubris, maybe we will dedicate a whole letter to that someday.

But it bears mentioning here, as a warning on leverage.

Back then, LTCM had about $1 billion in capital and exposures on positions (that we know of) through derivatives and massive leverage of over $100 billion.

And guess what set of trades was central to their epic meltdown? The meltdown that threatened to take down Goldman Sachs, half a dozen other investment banks, and more or less the entire US, and hence, global financial system?

US Treasury Basis Trade.

Now mind you, these were a different structure in that LTCM was buying off-the-runTreasuries (which were slightly cheaper due to being less liquid) and shorting the more expensive on-the-run Treasuries, expecting the price difference between them to decrease over time.

However, in 1998, the Russian government defaulted on its debt, leading to a global financial crisis and a flight to quality, where investors piled into US Treasuries.

They were buying on-the-run USTs like mad, making the price in those spike in relation to the less liquid off-the-run USTs.

LTCM's prize-winning economists' theories broke: spreads not only didn't converge, they exploded wider.

Word spread on the street and traders picked up on it like blood in shark infested waters, and they piled into the trades themselves.

In the opposite direction.

Any trade they heard that LTCM was in, they took the other side.

This pile-on caused LTCM to experience massive losses, huge margin calls, positions to be unwound at gigantic losses, and ultimately the collapse of the firm.

But the leverage.

Goldman and other banks' had massive exposure to LTCM, its balance sheet, its positions.

Counterparty risk led to contagion led to the imminent collapse of not just LTCM, but the larger financial system.

It required the NY Fed to orchestrate a total bailout of Goldman and other exposed banks by other major banks and financial institutions to stabilize the market and prevent a global meltdown.

Though LTCM still had a nuclear meltdown.

Risk happens fast.

But, could the same thing happen today?

This was one firm, not eight. And they were levered over 100 to 1, not 50, like the hedge funds today. And they were in a lot of other types of arbitrage trades that blew open in the market turmoil, not just the basis trade.

All true.

But let's address some of this.

First, whether it is one firm or eight, it's still just a handful of parties with a handful of counterparties that have consolidated risk to one section of the market. Sure it's the biggest section, but if one of them should fall, the ramifications would likely cause a cascading meltdown.

Second, even though the LTCM leverage was over 100 to 1, the amount of capital was one-tenth of the amount we are talking about in exposure here today. On just the basis trades.

Today's hedge funds likely also have massive exposures elsewhere that could be caused to blow out just like LTCM's did when the Street heard about the problems they were having. If a hedge fund blows up, it's not just the basis trade that implodes, causing cascading effects there, it is also likely many other trades and exposures that would certainly impact other counterparties, including their own prime broker, other banks, and other funds.

Counterparty risk.

This, in turn, is exactly what causes contagion.

The knock-off effects of the failure on a single counterparty, causing other counterparties to fail with far-reaching and spidering causation.

However.

We already have mitigating factors in place to prevent this very thing from happening again.

First, when the basis trades began to blow out in March of 2020, the Fed and Treasury stepped in ensuring sufficient liquidity in Treasury and mortgage markets, as well as equities, of course.

This not only prevented any failures, it basically guaranteed returns for the large hedge funds who had exposures to basis trades.

The Fed Put.

Also, the Treasury has already announced that they are instituting a regular buyback program to ensure liquidity in off-the-run US Treasuries in 2024.

This basically puts a floor on the price of the Treasuries that hedge funds are long in their basis trade, preventing massive losses.

What a deal.

Still, there is no absolute guarantee that there will be timely and sufficient bailouts to prevent any market shocks in the future that may emanate from these massive basis trades.

There is always the possibility of a black swan event that causes the market to act in unexpected and difficult to predict ways.

We could easily see a scenario similar to the LTCM crisis, factors that could converge to create a perfect storm.

For example, a sudden, unexpected economic event could lead to a flight to quality, drastically changing the demand for Treasuries and affecting their prices. If the market simultaneously experiences high volatility and liquidity issues, funds holding highly leveraged basis trades might find themselves in a position similar to LTCM, facing large, rapid losses with limited ability to exit their positions.

They could face a dearth of liquidity for their repo borrowing.

A major bank could collapse that leaves one or more of them exposed to short-term liquidity crises.

Do I expect this?

No.

Could it happen?

Absolutely.

I lived through the LTCM debacle as a merger arbitrage trader that year. I watched as our trades and spreads blew out on the backside of the LTCM implosion.

We stomached and weathered the pain, wondering when it would end.

But because we were positioned responsibly, we had plenty of capital on the sidelines, ready to deploy in these spreads when they blew open.

We were able to take advantage of the mis-priced opportunities, the market confusion, the inefficiencies.

Because we were well-diversified, we were safe. In fact, we were better than safe.

And so, with the markets seemingly priced to perfection from equities to bonds, I am taking a similar approach as we had in 1998.

My own portfolio is well-diversified across asset classes and sectors. I am sitting on plenty of cash and short term USTs. And though I hope we don't experience some sort of black swan or market shock event, I am ready.

I strongly suggest you do the same.

Then crack open that champagne, put the prime rib in the oven, and celebrate the holidays with absolutely no worries at all.

That’s it. I hope you feel a little bit smarter knowing about the basis trade and how hedge funds are using it.

If you enjoyed this newsletter and found it helpful, please share it with someone who you think will love it, too!

Talk soon,

James✌️