What is the Sahm Rule Telling Us?

What is the Sahm Rule Telling Us?

Issue 93

✌️ Welcome to the latest issue of The Informationist, the newsletter that makes you smarter in just a few minutes each week.

🙌 The Informationist takes one current event or complicated concept and simplifies it for you in bullet points and easy to understand text.

🫶 If this email was forwarded to you, then you have awesome friends, click below to join!

👉 And you can always check out the archives to read more of The Informationist.

Today's Bullets:

Who is Claudia Sahm?

What is the Sahm Rule?

What's Sahm saying now?

Two Big(?) problems

Inspirational Tweet:

The Sahm Rule. Something we have been hearing about a little bit more lately, and I expect to hear a whole lot more soon.

But what exactly is the Sahm Rule? How does it relate to recessions? And is it as accurate of an indicator as it is claimed (or sometimes hyped up) to be?

Important questions that we will tackle here, nice and easy as always, today. Glad you brought it up Eric, thank you for this week's Inspirational Tweet.

So, grab that cup of coffee, saddle up, and settle in for a short ride into economist land with The Informationist.

🧐 Who is Claudia Sahm?

First, as we know, academically created principles, rules and laws are typically named after a person (often the creator), such as The Pareto principle (80/20 Rule) developed by Italian economist Vilfredo Pareto, or Gresham's law (bad money drives out good) created by Henry Dunning Macleod, who decided to name the law after Sir Thomas Gresham.

The Sahm Rule was created by and named after Claudia Sahm.

Who is that, you may ask.

Let's see.

Claudia Sahm is an American economist known for her work in macroeconomics and household finance. After graduating from Denison University in 1998, where she studied political science and German, she worked at the Brookings Institution as a research assistant from 1999 to 2001.

For those wondering, Brookings is a think tank, which does research and analysis for public policy.

And think tanks are basically research consultants for the US Government.

After her stint with Brookings, Sahm then went to The University of Michigan, where she studied towards and received her PhD in Economics after six years.

Upon graduation, in 2007, Sahm became an economist at the Federal Reserve Board of Governors in DC. She held several roles and was promoted over the course of her 12-year tenure, where she eventually became the Section Chief in the Division of Consumer and Community Affairs.

In May 2019, Sahm introduced the Sahm Rule in a report called "Recession Ready: Fiscal Policies to Stabilize the American Economy," which was published by none other than...?

The Brookings Institution.

You see how this all works, right?

In any case, the Sahm rule has become a Fed-respected tool for understanding and possibly responding to economic conditions, particularly the onset of recessions.

And it does this by looking at unemployment numbers.

Let's dig deeper.

🤓 What is the Sahm Rule?

Put simply, the Sahm Rule is a simple calculation based on the unemployment rate.

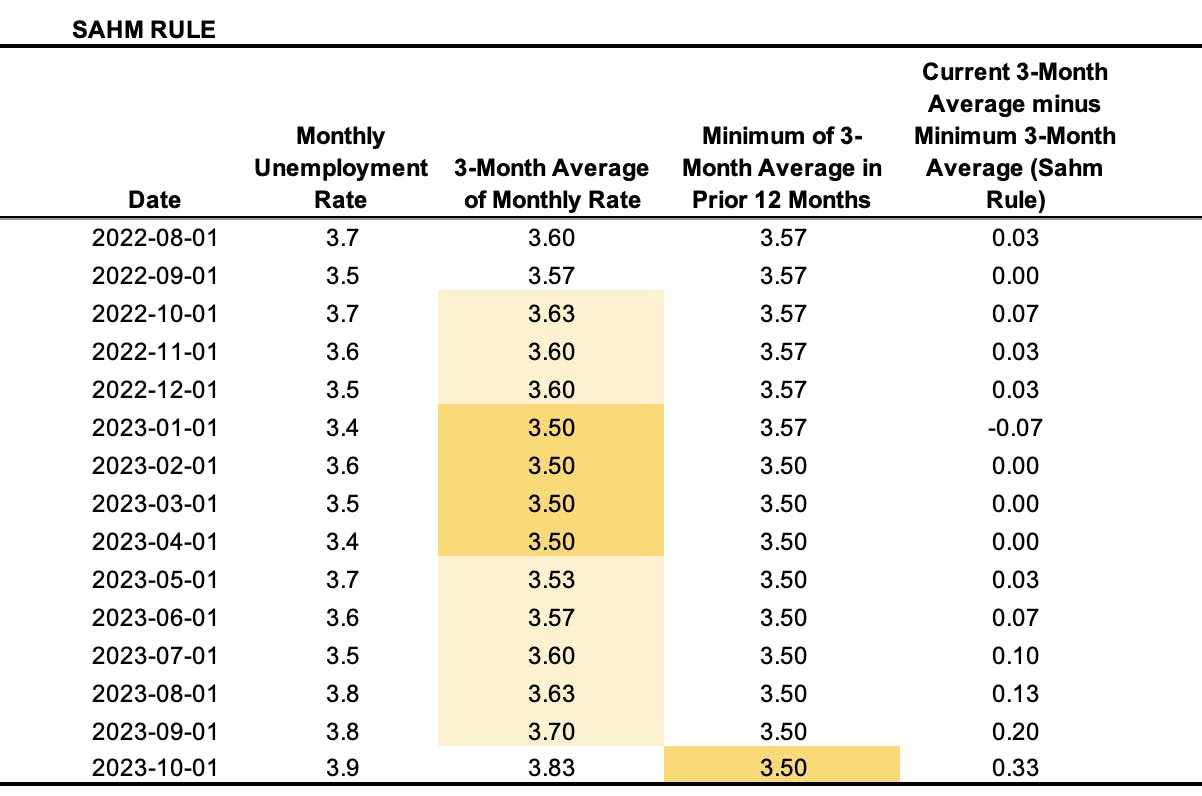

The rule says: a recession is signaled when the three-month moving average of the national unemployment rate rises by at least 0.5 percentage points above its low during the previous 12 months.

That sounds confusing in words, so let's peek at the actual numbers and work through it together.

Looking back over the last year, we first calculate the 3-Month Average of the Monthly Unemployment Rate. Looking at the previous three months up to the October reading, we get an average rate of 3.83.

Next, we look at the Lowest 3-Month Average Rate over the prior year. So, looking at the last year, the lowest average was 3.50%, which it held for four months before ticking back up again. This has been the lowest average for the last nine months.

Remember that.

Now we look at the Current 3-Month Average versus the Lowest Rate over the last year.

Because the rule says a recession is signaled when the three-month average unemployment rate rises by 0.5% or more above its low during the previous year, and the current rate is only .33%, according to Sahm and as of October, we were not yet in a recession.

This seems to make sense. By looking at the rate of change, rather than the absolute rate itself, and the difference between that average rate and the rate at the lowest point of the cycle, we can see from 100,000 feet up what is going on with the economy.

Notably, Sahm uses the three-month moving average in the Sahm Rule which helps to smooth out short-term fluctuations and possible anomalies in the unemployment rate.

Like massive hiring for holiday seasons or layoffs from a large union (think: United Auto Workers).

This makes the rule a more stable and reliable indicator of significant and sustained shifts in the labor market that could signal the start of a recession.

Using Sahm's own words: The logic of the Sahm rule is that when the unemployment rate starts rising, it often picks up steam, and we get a recession. A key input to the rule is the lowest value of the 3-month average (dark yellow in the previous chart) in the prior 12 months (light yellow).

OK, I can think of a couple of problems here, but we just got a fresh set of unemployment numbers on Friday, so let's plug them into the formula and see at what Sahm's Rule is telling us about any incoming recession first.

🫣 What's Sahm saying now?

First, in somewhat of a surprise to economists and Wall Street, the unemployment number decreased from last month's reading.

It went from 3.9% unemployed in October to 3.7% in November.

This, of course, caused the 3-month average rate to drop from 3.83 to 3.8, and so the difference between that and the lowest rate over the last year of 3.5%, also decreased to .3% from .33%.

Nowhere near the stated .5% gap needed to signal a recession.

So, it seems, we are in the clear for now, no recession, no problem.

Well.

There are a ton of qualifiers that many professionals are attaching to this past unemployment number, not withstanding large swaths of government hiring and re-onboarding of striking employees with the United Auto Workers union reaching agreements with the Big Three Auto manufacturers.

In fact, Healthcare added 77K, Government added 49K jobs, and manufacturing, 28K (UAW strike ended), Leisure and Hospitality (think: restaurants and bars) added 40K.

However, Retail lost 38K jobs and transportation and warehousing cut 5K. This, plus employers brought on fewer temporary workers than usual this holiday season.

Seems the Government filled that hole completely, though, and then some.

As for where we are going, it does seem the Sahm Rule remains intact, and we are not yet headed into a recession.

But back to the data and a few nitpicks from this professional investor.

🤨 Two big(?) problems

First of all, the absolute value of .5% of change off the lowest unemployment value seems arbitrary to me.

It clearly doesn't not give a false positive indication, but it often overshoots the mark.

For instance, we had a low of 2.53% unemployment back in 1953, and the recession kicked in when the rate jumped to just 2.6% in July of the same year, according to the Fed of St. Louis (FRED). But the Sahm Rule didn't kick in until October of 1953, a full 3 to 4 months after the recession had begun.

This happened in a number of other places, as you can see on the chart below. The red line is the .5% 'indicator' threshold.

Perhaps if Sahm used a velocity measure, (i.e., the rate of change from month to month averages), rather than just a fixed change from the lowest point, this would address the issue.

Bottom line, .5% is a 20% move from the bottom of of 2.5% (the lowest unemployment value for that 1953 period).

Flash forward to the late 1980's, early 1990's, and the lowest value was 5.3%.

So, a .5% move from that bottom would only be a ~9% move higher in unemployment.

While I understand that part of the importance and elegance of the Sahm Rule is simplicity—something we are all about here at The Informationist—I also believe that this measure could be refined a bit.

Especially since The Fed seems to be using it as one of their key unemployment indicators for monetary policy decisions.

I'll do more work on the velocity idea, nonetheless, and get back to you.

Secondly, and perhaps loosely related to the above observation, it seems the Sahm Rule is less of a leading indicator and more of another lagging indicator.

After all, charting out the Sahm Rule versus actual recessions, we see that virtually every recession starts before the Sahm Rule is actually triggered. And some (red arrows above) start months and months before.

So, if this is an important tool for the Fed to make decisions around interest rates and quantitative tightening/easing, it seems more than a bit problematic.

I've said it many times before, and so a number of you have heard this, but I will say it again.

Loudly for the ones in back.

The unemployment rate is a terrible predictor of a recession, but a wonderful confirmationonce we are in one.

Just look at how the unemployment number spikes after (sometimes well after) we enter a recession.

Admittedly, I'm no PhD Economist, but I suggest we all take the unemployment rate and even the Sahm Rule with a hefty dose of salt.

Nothing against the Sahm Rule, it certainly has its place and uses.

But as far as I can tell, predicting and measuring the actual onset of a recession?

This is not one of them.

The sinister investor in me thinks: The Fed and its economists know all too well that they have little choice but to put you and me and anyone else they need to out of a job in order to crack inflation, cause some temporary deflation, and start the whole cycle again.

The employment reset button.

But they will continue to point to the actual lagging unemployment rates and lagging measures like the Sahm Rule in order to get what they want and need without admitting that they knew that you and others would be employment casualties all along.

So, maybe it's time we stop looking at unemployment as an indicator of a coming recession.

Shall we?

That’s it. I hope you feel a little bit smarter knowing about the Sahm Rule, how to read it yourself, and just how useful it is for predicting a recession.

If you enjoyed this newsletter and found it helpful, please share it with someone who you think will love it, too!

Talk soon,

James✌️