0DTE Options: Will They Cause A Market Avalanche?

0DTE Options: Will They Cause A Market Avalanche?

Issue L

✌️ Welcome to the latest issue of The Informationist, the newsletter that makes you smarter in just a few minutes each week.

🙌 The Informationist takes one current event or complicated concept and simplifies it for you in bullet points and easy to understand text.

🧠 Sound smart? Feed your brain with weekly issues sent directly to your inbox:

Today’s Bullets:

What’s a 0DTE?

Who Trades 0DTEs?

How do 0DTEs affect the market?

Could 0DTEs cause a market avalanche?

Inspirational Tweet(s):

and…

0DTE. That strange acronym seems to be popping up everywhere recently. No surprise, as zerohedge points out above, the volume of 0DTE activity has skyrocketed the last two years.

But what exactly are 0DTEs, and are they really an issue, Matteo Marinelli suggests?

No worry, The Informationist has your back on this one. Let’s break it down and build it up, nice and easy as always, shall we?

The Informationist is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber. And so you know, this is the last chance to upgrade at the discounted price. The price goes back to the normal $15/month, $150/year price tomorrow.

🙏 Early supporters get 33% off for the first year — just $100, or $10/month ✌️

🧐 What’s an 0DTE?

To understand 0DTEs, we must first review the basics of options. The options we’re talking about today are simply the right to buy or sell a listed security at a certain price that expires on a certain day.

For example:

If you buy a February 17th $130 Put in AAPL, this would mean you own the right to sell 100 shares of AAPL (a single option contract represents 100 shares) at $130, and this right expires on February 17th.

Likewise, if you buy a February 17th $130 Call in AAPL, this would mean you own the right to buy 100 shares of AAPL at $130, and this right expires on February 17th.

A few terms for you today:

Strike Price → this is the price of the security that you are trading the right to buy or sell it at (i.e., $130, in the example above)

Premium → this is the cost of the option itself

Expiry → just as it sounds, this is the day the option expires

Contract → options trade as contracts, and each contract is ‘the right to buy or sell 100 shares worth’ (if I buy 5 February 17th $130 Calls in AAPL, this is 5 contracts, or 500 shares worth)

In the Money → the option is trading at a price that is already profitable for the buyer (if I buy a $120 Call in AAPL and the stock is trading at $130, then the option is $10 in the money)

Out of the Money → just the opposite, this is the amount an option is away from being profitable to the buyer (if I buy a $140 Call in AAPL and the stock is trading at $130, then the option is $10 out of the money)

Simple, right?

OK, so what does this have to do with the whole 0DTE business?

Well, 0DTE stands for Zero 0(Zero) Days To Expiration. In other words, it refers to options traded on the market that are expiring on the same day of trading.

I.e., options trading on February 6th that are also expiring on February 6th are 0DTEs.

Options trading on February 6th that expire on February 7th are 1DTEs,

Options trading on February 6th that expire on February 8th are 2DTEs,

and so on…

Now you may ask, why would someone want to trade options that are expiring on the exact same day they are trading them. Seems rather pointless, as one of the main components of an option’s value is time to expiration (the other two being the option’s strike price and the volatility of the underlying security).

One might even say that it seems akin to buying a lottery ticket or placing a bet in the 4th quarter of an NFL game.

If they’re about to expire, what’s the point?

🤑 Who Trades 0DTEs?

As you know, there are two main categories of investors: institutional and individual (retail). And within each of those categories, there are two types of investors who trade the majority of 0DTEs: those who are hedging (removing risk) and those who are speculating (i.e., betting, or adding risk).

So, we have:

Institutional hedging

Institutional speculation

Retail hedging

Retail speculation

There far fewer institutional speculators, but they are far larger than individual speculators.

And while the individual speculators may be smaller in trade size, there are far more of them out there than institutions.

Case and point is the short-squeeze melt up of stocks like AMC, GME, BBBY experienced in 2021, where Reddit-using retail investors swarmed and overwhelmed institutional short sellers, helping coin the term Meme Stocks.

So, don’t make the mistake of merely dismissing the day traders out there, because while they may be smaller individually, collectively they pack a hell of a punch.

Unpacking these, this is how the various parties typically trade 0DTEs:

A retail or day trader most likely trades 0DTE options because they allow him to speculate or make large bets on positions quickly and require much less capital than buying entire blocks of ETFs or stocks.

Remember, all options are derivatives, and they are all inherently leveraged trades.

You don’t have to buy 100,000 shares of AAPL to get the benefit of the 1,000 shares of the stock’s volatility, you just have to buy the 100 options to buy or sell the shares. And that costs a fraction of the total cost of buying that much stock.

While there are some who use 0DTEs for portfolio insurance, by and large, most retail traders are just speculating on the price of stocks over the course of a day.

And while largest numbers of institutions are likely using 0DTEs for hedging or portfolio insurance, the ones who do use them for speculation are typically large hedge funds who have massive amounts of capital at their disposal and can move even the largest and most liquid ETFs and stocks.

After all, 10,000 calls or puts at .25c per contract is just $250,000.

Literally a drop in the bucket for a $10 billion hedge fund.

They can speculate, manipulate, and move markets with their sheer size and ability to spread trades across the street using different dealers (brokers).

We’ll get into that a bit more later.

But first, the last major category of traders using 0DTEs are those using them for hedging purposes.

Say a large institution, like the University of Texas endowment, own 100,000 shares of AAPL stock. And let’s say that AAPL, which is trading at $150, is about to announce earnings, where they reveal just how many new model iPhones they sold. If UT is worried that sales may be less than expected, they may want to hedge some of that risk. One way they could do this without selling shares before the earnings announcement is to buy puts, just in case the announcement is dismal.

Since there is not much time premium embedded in the price of the 0DTE AAPL options, they could get some quick insurance by buying some out of the money puts.

If they buy 1,000 $145 AAPL 0DTE puts which cost them 1.50 per contract, or a total of $150,000, then they have just paid a 1% premium for insurance against a total collapse in AAPL price.

$1.50 x 1,000 contracts x 100 shares per contract = $150,000, or 1% of the $15,000,000 of stock they own

In effect, UT would limit their total possible loss on APPL stock to $6.50 per share ($5 price drop + the $1.50 price per share in insurance).

On the other side of this trade, the one who is selling UT this insurance, is most likely an options dealer at a large bank (another institution).

But why would a dealer sell this insurance? Wouldn’t they effectively be long the stock if they had to buy it from UT in the case of a collapse in earnings and price of AAPL? All just to collect a fee of $150,000?

Short answer is yes.

If the stock remains stable and does not drop below the strike price of $145, then the dealer collects his $150,000 and calls it a day. But if AAPL disappoints and drops below $145, then the dealer would be on the hook for 100,000 shares, as they say on Wall Street.

For instance, if APPL stock dropped to $125, the dealer would lose $2,000,000 versus the mere $150,000 option premium he collected.

oops.

That is, if he did nothing to protect himself from that loss.

And this, my friends, is where something called delta hedging comes into play.

And this is exactly how 0DTE’s can move markets.

🤨 How do 0DTEs affect the market?

See, when a dealer sells 0DTEs to either speculators or hedgers, they have to then turn around and protect themselves on the trade.

Here’s how.

Dealers run books of positions using the bank’s money, known as proprietary capital, and hence these dealers are known as prop desks.

The prop desk’s job is to facilitate trades (i.e., take the other side of the customer to make the trade happen) and collect enough fees in commission and premium to make it worthwhile and hopefully cover any losses that are incurred from taking the other side.

They have effectively assumed risk to sell insurance to the buyer of the option—not too different than AIG selling flood insurance to a homeowner in Baton Rouge.

In the case of 0DTEs, if that flood insurance expired at the end of that same day.

And selling that insurance could actually cause a flood to occur.

Delta.

See, dealers use a book hedging strategy called delta hedging. An option’s delta estimates how much its value may change with a $1 move in either direction of the underlying security.

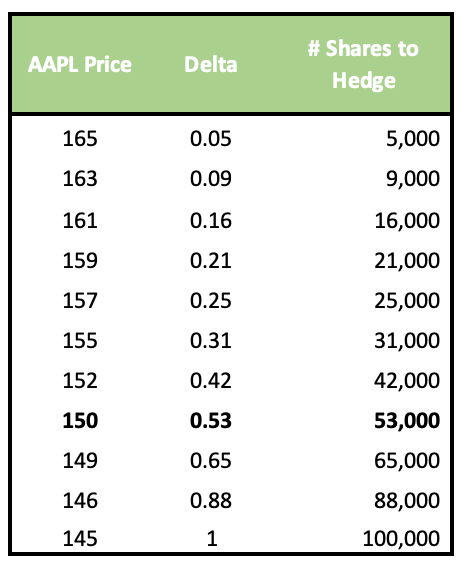

So, if the delta of the AAPL $145 Puts in the example above was .53, then for every $1 that AAPL fell in price, the option value would increase by .53c. The delta increases as AAPL price approaches (gravitates to) that $145 level, until it final reaches 1.0. From that point and lower, with every $1 that AAPL drops, the option becomes worth $1 more.

For example, let’s pretend that AAPL’s $145 Puts Delta table looked like:

The dealer might initially delta-hedge the calls in our scenario by shorting 53,000 shares (.53 X 1,000 puts X 100 shares per put). As the price of AAPL rises or falls, the dealer will adjust the the number of shares it is short, accordingly.

If the price moves up to $155, the dealer would cover some of his short until he was short 31,000 shares, and if it moves lower to $149, he would short more to be total short 65,000 shares.

So, if UT was right, or a hedge fund had speculated correctly, and AAPL fell in price as the day marched on, the dealer would be forced to sell more AAPL shares, according to normal risk management policies.

The further AAPL falls, the more the dealer must sell.

All the way until $145, where he has to be short the entire position to cover himself.

In other words, as the price gravitates to that option strike price of $145, the selling pressure increases dramatically, only pushing the delta even higher.

That very selling causes more selling.

So, as more and more traders and speculators pile onto the momentum and drive up the volume of 0DTE options, they also cause unnatural intra-day market moves around those option prices.

Question is, can this activity cause something to break?

😱 Could 0DTEs cause a market avalanche?

We’ve all seen how trading algorithms, programmed to read market activity, volumes, and directions of movements to make instant trades, try to capitalize on perceived imbalances or inefficiencies in the market.

To capitalize on momentum.

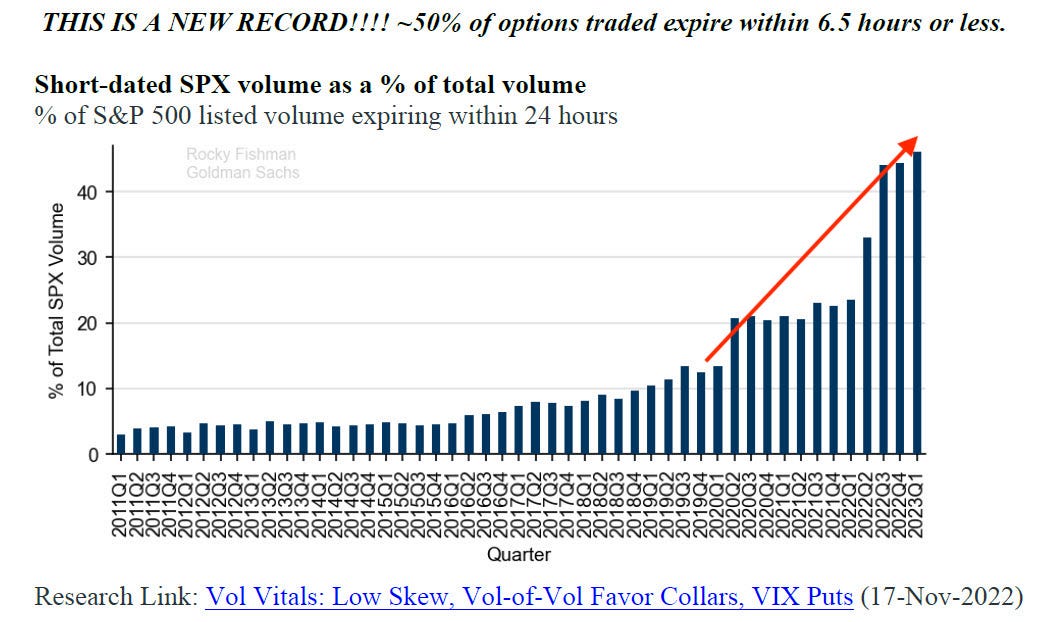

Going back to the first Tweet of Inspiration today, look at the sheer pickup in volume of the so-called 0DTE options in the last two years alone:

What this is saying is, that 50% of all SPX listed option trade volumes are in 0DTE options.

Whoa.

Remember Flash Boys by Michael Lewis, the story al about the flash crash caused by the now-infamous High Frequency Traders? Well, there’s a lot of controversy around whether or not the traders themselves caused the crash, but there’s little question that the HFT algorithms that traded millions of shares in literally nanoseconds contributed heavily to the stock market crash in May, 2010.

The HFTs traded on the momentum, causing automatic institutional-sized algo’s (or algorithms) to just generate more momentum, triggering more HFTs, triggering more algo trades, until…

*boom*

Major indices plummeted 5-6% in minutes, as a cascading effect occurred, creating a snowball that gathered and grew into an avalanche before anyone knew what had happened.

Could that happen again?

Well, there are rules and regulations that help prevent the same exact thing from happening again. But now we have a new algo, speculative, momentum-driven game in town.

And it’s called 0DTE.

So, what can you do about it?

You can pay attention to the activity of the options in the stocks that you are invested in, keeping track of strange movements, and if you are a long-term investor, understand the pricing on expiration days and avoid getting sucked into a gravitational pull of that strike price when adding to or selling off a position.

And if you are going to day trade for any reason (I don’t recommend this strategy, personally), be super aware of what’s going on in your 0DTE markets.

Because until they are either reigned in by the regulators or they cause the next market avalanche, they’re only going to affect the market more and more.

And more.

That’s it. I hope you feel a little bit smarter knowing about 0DTE and how they can affect what’s going on in the market and your favorite stocks.

Before leaving, feel free to respond to this newsletter with questions or future topics of interest. And if you’ve found The Informationist to be valuable, or just want to support the work I’m doing, consider subscribing. It would mean a ton to me. 🙏

✌️Talk soon,

James