30-Year Treasuries → Why Are Yields Spiking?

30-Year Treasuries → Why Are Yields Spiking?

Issue 77

✌️ Welcome to the latest issue of The Informationist, the newsletter that makes you smarter in just a few minutes each week.

🙌 The Informationist takes one current event or complicated concept and simplifies it for you in bullet points and easy to understand text.

🧠 Sound smart? Feed your brain with weekly issues sent directly to your inbox:

Today’s Bullets:

Reality of ‘risk free’

Why are yields spiking?

What are the implications?

What should you do?

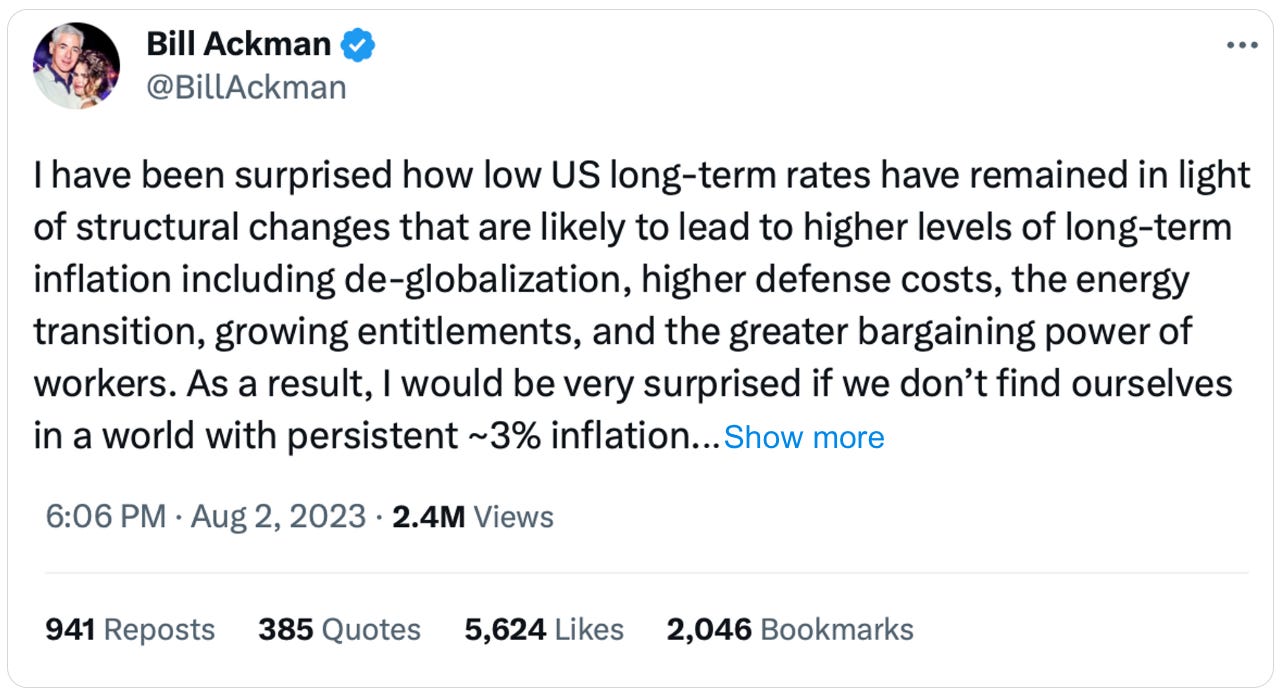

Inspirational Tweet:

Well, I understand Bill Ackman is quite polarizing for investors. But if you just focus on his words here (please click on the Tweet above to see the entire post), he makes some important and strong points about US Treasuries.

Long-dated Treasuries, in particular.

And, if you have not yet noticed, Bill was right about the mis-pricing of USTs, especially the 30-year (notice the date of his post, 2 weeks ago).

But why was he saying rates are too low, and what are the implications of the observation?

Super important questions, I believe, ones we should be asking and answering today.

And so, if bonds scare you and this all sounds complex and confusing, you’ve come to the right place. We’ll get you all sorted out, nice and easy as always, here today. So grab your favorite mug of coffee and settle in for a few minutes with The Informationist.

Join the Informationist community for access to subscriber-only posts, ask questions and participate in comments with other awesome 🧠subscribers + exciting new features on the way!

Partner spot

Some of you have been asking recently what I read in the morning for fast, digestible news, and I’m happy to report that my new favorite source, hands down, is 1440.

The folks at 1440 scour over 100 sources every morning so you don't have to. You'll save time and start your day smarter. What more could you ask for?

Sign up for 1440 now and get your first issue, immediately. It's completely free—no catches, no nonsense, and absolutely no BS. I wouldn’t recommend it, if I wasn’t sure you’d love it, too.

Join 1440 for free today.

🤨 Reality of ‘risk free’

Before diving in here, a quick primer on bonds and Treasuries, what they are and how they work. For those of you who are comfy with this part, feel free to jump ahead.

But if you want a bit of a tune-up, let’s proceed.

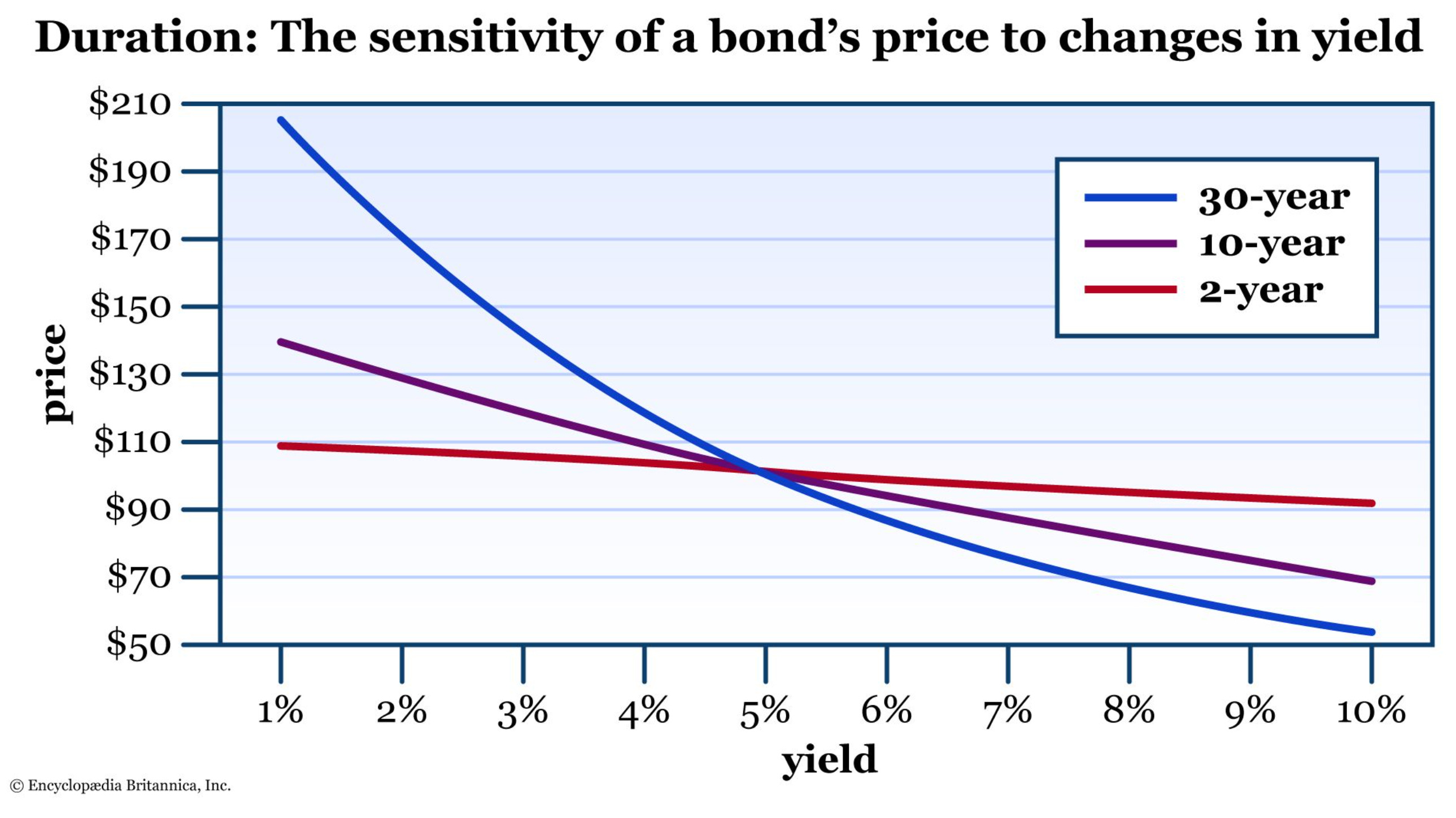

First, bond prices are a function of both yield and duration. If interest rates rise, then bond prices fall to compensate for that move in yield. And vice-versa. The longer the duration, the more sensitive the bond price is to the interest rate move, i.e., the more the price will rise or fall to compensate for that interest rate move.

This is the mark-to-market function of bonds.

In the case of US Treasuries, they are issued in an auction and then they are free to trade on the open market.

But if yields rise or fall after a bond is issued, then the market price of that bond is adjusted to reflect the change in the going rate or effective yield of that bond.

And, as you can imagine, if a 1-month T-Bill is issued at 5% yield, and then two weeks later the Fed raises rates by .50%, the price of that bond will only decrease by 2 or 3 basis points (2 or 3 hundredths of a percent).

But if this was a 2-year note, the price impact would be more, even more than that for a 10-year bond, and if it was a 30-year Treasury, the impact would be quite large, as you can see below.

All of that said. If you were to hold the bond you bought in auction (or at the earlier and lower yield in the open market) until maturity, then these price moves will not matter to you.

You will receive the rate that you purchased the bond at, period.

But in this case, you still have two risks:

The risk that you need liquidity before the bond matures and you must sell your bond at a loss.

The risk that inflation runs higher than the yield you are receiving over the life of your bond, creating what we call a negative real rate of return (we will revisit this below).

And so, even US Treasuries, the global reserve asset are not without risk.

They are, in fact, not risk-free.

Fitch (and S&P) Ratings know this, and investors know this, too. And they have adjusted to account for these risks, among others.

Let’s unpack further, turning to current pricing.

😮 Why are yields spiking?

A little reality check and why I posted this yesterday:

What you are seeing here is an increase in the yield of the 30-year UST from 4% to about 4.4% or 40bps so far, this month. That’s a 10% relative move in the yield, and even though it’s only .4%, it pushes 30-year USTs down as much as 6.5% in mark-to-market price.

“Risk-Free”, right? 🙄

Getting back to the reasons for this re-pricing, let’s visit some of the glaring and obvious ones.

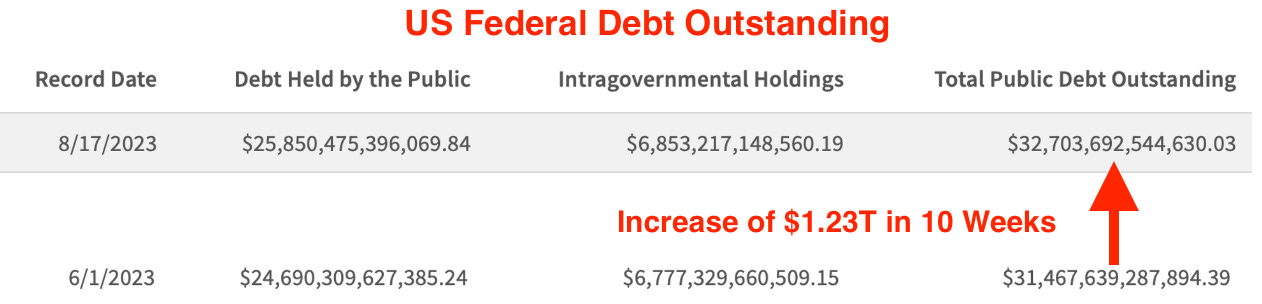

If you’ve been watching, you know we’ve seen a few key developments in the US government financial position recently. First, a decrease in tax receipts of approximately 7.3% from one year ago.

Then, an increase in spending from $4.83T to $5.30T thus far in the fiscal year, which represents a 9.7% increase YTD (remember, the federal fiscal year runs from Oct to Sept).

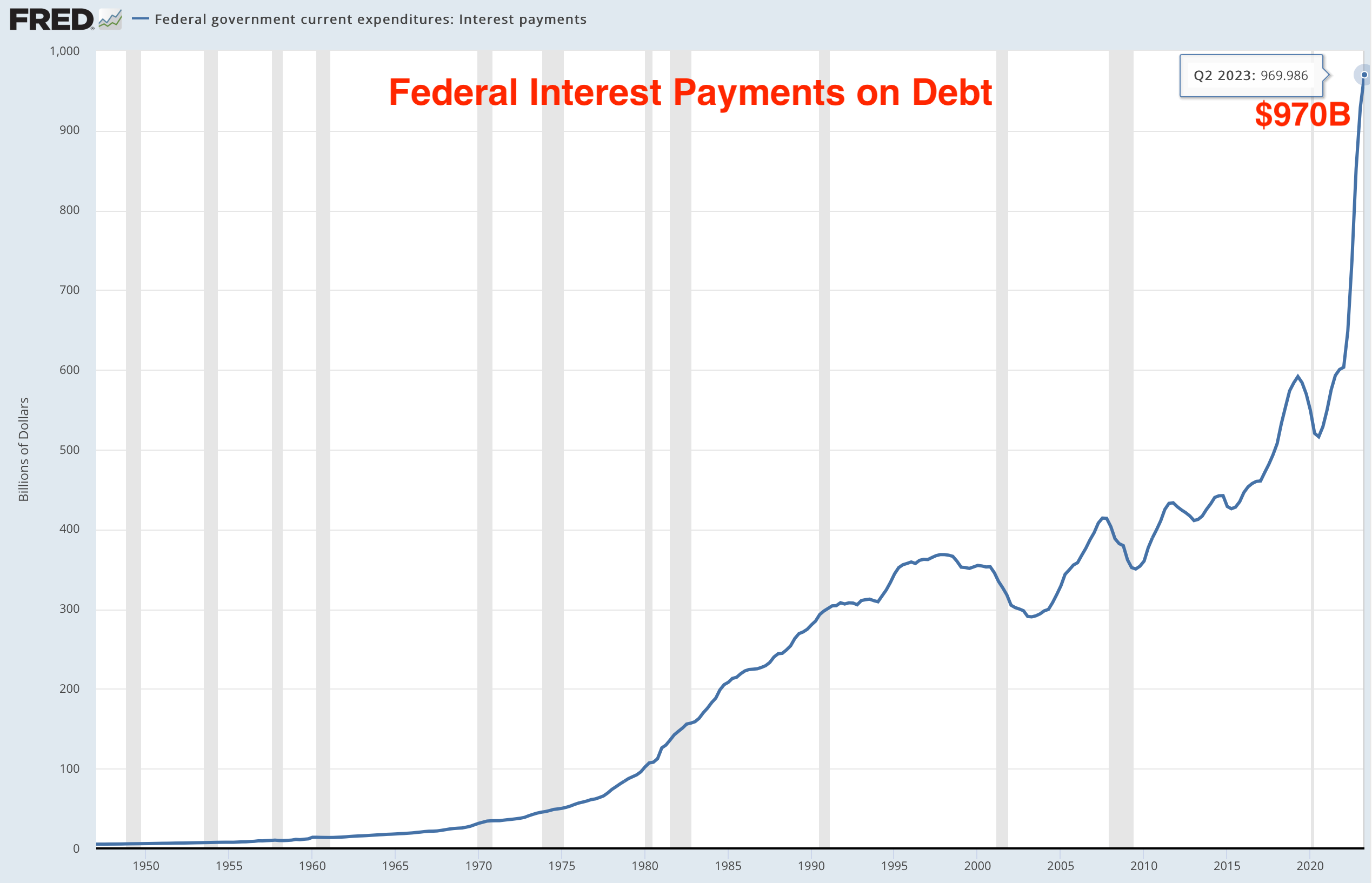

And this is almost certain to just get worse. Because of this:

Which is leading to this:

In other words, the US Treasury finds themselves in the dreaded debt spiral, something I’ve written quite a bit about in past newsletters and on Twitter.

But to simplify for new readers:

decreased tax revenues → leads to higher deficits → and more borrowing (debt) → and more interest payments → leading to even higher deficits

And this is all exacerbated by higher rates → leading to even higher deficits

Bottom line, the US Treasury is going to have to issue a massive amount of debt to cover growing deficits.

Mountains of it. 🏔️ (or maybe we should us this: 🌋)

In any case, the deficit is set to be $1.39T for the first 9 months of this fiscal year (up 170% from last year). The problem is that they now need to issue even more debt at a time that foreign appetite for US Treasuries is decreasing.

This is mostly due to Russia dumping virtually all their USTs, and a significant decrease in demand from both China and Japan, as they are both selling USTs and then the USDs they get for them to buy their own currencies these days.

Adding fuel to the fire, we have the recent credit downgrade in US debt by the ratings agency Fitch.

And while Fitch’s move is significant IMO, I don’t believe this has had a huge impact in and of itself. However, it did serve to place a huge spotlight on the US debt situation and has emboldened investors to demand higher yield at the long end of the curve.

I wrote all about this downgrade in a recent newsletter that you can find here:

Back to the demand of 30-years Treasuries, it has simply become a supply and demand equation.

The US Treasury, as noted above, has floated over $1T of paper in the last month or so. The bulk of this issuance has been at the short end of the maturity ladder, as the Treasury has been issuing mostly T-Bills, maturing in a few weeks or months at most.

They did this to tease some cash out of the Reverse Repo Facility that had over $2T sitting idle in it. And it worked. For now.

But they are continuously coming back to the till to re-issue more debt as this paper quickly matures. At some point, they must issue longer maturities, something they began to do this past week.

Come year-end, I expect the Treasury to ramp up these longer-maturity offerings, pretty much flood the market with them.

And investors clearly expect this, too, demanding higher rates, ad they want to be compensated for the coming Treasury load and higher long-term inflation risks.

🫣 What are the implications?

See, as the Treasury continues to add to the US debt load, digging a $32.7T hole, they must hope for (read: work with the Fed to ensure) higher structural inflation. This will lead to higher GDP, higher tax revenue, and hopefully a lower deficit in the future.

And so, if inflation is 3 or even 4% instead of the old-target 2%, then longer dated 30-year Treasuries would settle in at the 5 or 6% yield level.

That’s a possible move of another 36% relative to the current 4.4%.

Yikes.

And let’s not forget about the other elephant in the room, the 30-year US mortgage, which is priced off the 30-Year Treasury.

This guy is looking nasty these days, higher than I’ve seen in over 20 years, in fact:

And so this will continue to weigh on the available inventory (I mean, who wants to sell their house with a 2.5% 30-year mortgage to go buy another house at 8%?).

Context for a 20% down on a 30-year mortgage:

A $300K house at 2.5% = $60K down and a monthly payment of $948

A $300K house at 8% = $60K down and a monthly payment of $1,761

Ouch.

🤓 What should you do?

First of all, if you don’t have to, you probably should not sell your house with a 2.5% mortgage rate right now.

Also, I’ve been saying this for a number of months now, I believe there is an elevated risk of a credit event due to the rapid rise of interest rates this past year. One that could cause a severe market drawdown.

For this reason, I hold a large percentage of my portfolio in cash and short term USTs.

The cash in my portfolio is in a fully FDIC+ insured money market instrument that yields the equivalent of a blend of T-bills and short Treasury Notes.

I personally do not own any long-term bonds.

If you do not have access to a money market account that offers attractive rates (I know some E*Trade and other trading houses do not offer this), then you can use the BIL ETF as a pretty good replacement for T-Bills.

Otherwise, you can likely buy USTs in the market. I would personally be sure the maturities are quite short, however. The drawback here is that you must keep re-investing as they mature and this can get tedious for those of you who are busy.

And finally, you can buy US T-Bills (and other bonds) directly from the US Treasury. Just go to TreasuryDirect.gov to open an account.

Because even though the 30-year Treasury is nowhere near ‘risk-free’, the 30-day US T-Bill is about as risk-free as you are going to get these days.

As for me, I want to be ready with plenty of powder in the increasingly likely scenario that we soon get a market disrupting credit event.

And being ready may make all the difference.

That’s it. I hope you feel a little bit smarter knowing about Treasuries and especially the 30-year. Before leaving, feel free to respond to this newsletter with questions or future topics of interest.

And if you are a paid subscriber, don’t forget to leave a comment or answer a comment in our awesome 🧠 Informationist community below!

Talk soon,

James✌️

Great post James, as always. My Sunday morning coffee always made better with a good dose of the Informationist.

A pro-tip 🤜 and build around your point of investing in short-term T Bill for the busy person: I have mine on “automatic” reinvestment. This is a simple elective through the Treasury Direct website, and the elective is made prior to the purchase--so simple. Currently, I keep a bunch of dry powder in 1-month T Bills and on automatic reinvestment until things settle or a great opportunity pops up.

Also, short duration TBills are earning more than iBonds currently.... love the irony! 😏

Thank you for this!!! ...and instead of coffee, I listened to the article while on a run this morning 🏃🏽.

When you put out your tweet (or X?) the other day, I immediately went on ChatGPT to better understand why this happens: however, my prompt engineering skills can use some work. I immediately assumed a “sell off” of 30y, thus leading me down a rabbit hole as to why a sell off would occur (inflation concerns, monetary policy actions, market sentiment, etc.).

What your article made me realize is that yields can increase when the treasury issues more 30y bonds...which completely makes sense. They flood the market (“dilute the shares”) which brings prices down, yields up.

A few questions:

1) Does the treasury issue on the long end because of how banks traditionally work by buying on the short end and lending long?... or more so to try to lower the debt interest in the short term?...tor both?

2) Why do we look at speeds between specific parts of the yield curve (ie 2’s/10’s)?...why not look at a 1m vs 30y 🥸

3) Why is there a difference sensitivity of bond price to yield?...is that mainly due to time value of money?