ISDA and its Endgame - Part 2

✌️ Welcome to the latest issue of The Informationist, the newsletter that makes you smarter in just a few minutes each week.

🙌 The Informationist takes one current event or complicated concept and simplifies it for you in bullet points and easy to understand text.

🫶 If this email was forwarded to you, then you have awesome friends, click below to join!

👉 And you can always check out the archives to read more of The Informationist.

Today's Bullets:

Basel History

Basel II and the Update

Basel III and the Endgame

Inspirational Tweet:

The Basel III Endgame. We're starting to hear more and more about this concept and the regulations around it.

But what is the Basel III Endgame, and how is it related to this ISDA Letter business?

A quick aside:

If you're like me, when you hear the term 'Basel', you can't help but see an image of John Cleese as Basil Fawlty, the cynical, dry-witted and snobby hotel proprietor in the short British TV-series Fawlty Towers. Fumbling and bumbling about an old English hotel, making more of a mess than an upper class experience for his guests.

His wife Sybil constantly yelling, "Basil!" when cleaning up the wreckage he has left behind.

Perhaps apropos to the subject here?

Well today, we will dig a bit into Basel and its endgame in this Part 2 of the ISDA Letter, and just how exactly it is related to the ISDA Letter.

If you are new to the Informationist this week and have not read Part 1 of the ISDA Endgame from last week, you can find that here:

I encourage you to have a quick read of that one first.

All done?

OK, now you know that we keep it high-level and simple around here, with the main goal of understanding this complicated financial world.

So, grab a cup of coffee and settle into comfy spot for a quick Sunday read with The Informationist.

🧐 Basel History

A little backstory on Basel and its formation first.

See in 1974, the Herstatt Bank in German faced a nasty liquidation after an implosion caused by foreign exchange exposures.

These exposures led to Herstatt Bank being unable to settle its foreign currency obligations, which caused ripple effects in the global financial system.

Say it with me: Contagion.

I know, I know, it always starts with a crisis, doesn't it?

As if the bankers don't know exactly what they are doing with excess leverage and risk-taking just to create profits to line their own pockets.

It sometimes seems like they treat the financial world as a personal casino, but being bankrolled by their customers.

What a deal.

In any case, in response to this and other looming banking issues, the Basel Committee on Banking Supervision (BCBS) was promptly founded.

BCBS members were basically the central bankers and regulators from the original Group of Ten (G10) countries: Belgium, Canada, France, Germany, Italy, Japan, Netherlands, Sweden, Switzerland, United States

The BCBS operates under the auspices of the Bank for International Settlements (BIS) and is headquartered in Basel, Switzerland, hence the “Basel Accords.”

The BCBS mission?

"To develop international standards for bank regulation and enhance financial stability by improving supervisory know-how and the quality of banking supervision worldwide.”

Translated: To prevent another banking crisis or collapse like Herstatt Bank.

Uh huh. Bang-up job everyone. Well done, truly. 🙄

Regardless, over the course of the next decade, the G10 grew along with global risks of banking. The BCBS eventually became worried about a phenomenon known as credit risk.

Of course, the Black Monday stock market crash of 1987 occurred, and a savings and loans crisis was ongoing in the states.

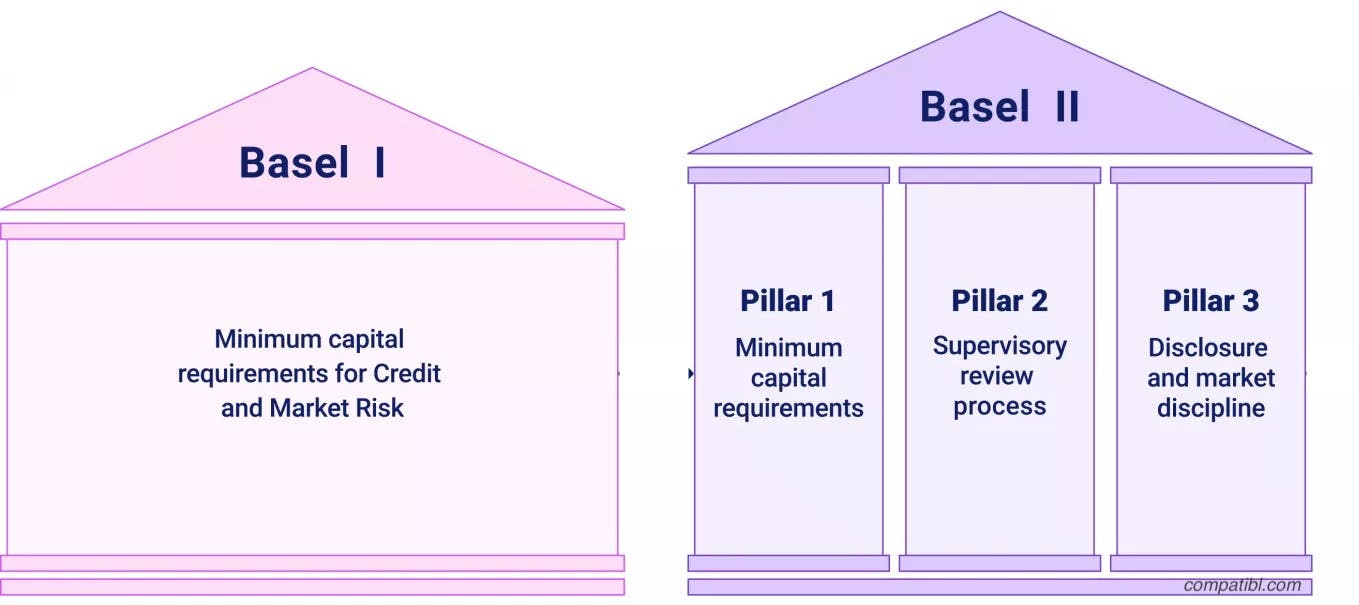

And so, in 1988, the BCBS created the Basel Capital Accord, a fancy term which was basically a classification system for bank assets.

The accord was know as Basel I.

Basel I focused on the capital adequacy of financial institutions, and established a set of rules for banks to mitigate risk and ensure financial stability.

Ensure.

I mean, I can't help but laugh as I write this. It's just comical, really.

But they did use some math and established requirements for banks.

Basel I Key Points:

Under Basel I, bank assets were classified according to their level of risk

Banks were required to maintain emergency capital based on that classification

The capital requirement was set at 8% of risk-weighted assets (RWAs)

Remember this key point right here: Under Basel I, bank assets were classified according to their level of risk.

We're going to revisit that one more closely next week.

🤨 Basel II and the Update

OK, so now that we have the BCBS operating under the Bank of International Settlements, with oversight from all G10 regulators and central bankers, problem solved, right?

Right?

Well, it seems the bankers remained one or two steps ahead of the regulators, BCBS and Basel I, constantly finding creative ways to introduce leverage and adding new tables and games to their personal financial casino.

In fairness, the BCBS did recognize this, and tried to keep up.

But outfits like Long Term Capital Management (LTCM) were far ahead of them, using brokerages and banks like their endless piggy vaults, and creating massive, interconnected leverage all over the banking system.

Then, a simple widening of credit spreads caused LTCM to literally implode, and like a giant collapsing star, it almost took all the banks and the global financial system with it.

Regulators will contend that Basel II was not created because of LTCM, but you better believe it was top of mind in its update.

After all, LTCM exposed significant risks to the global financial system due to its extensive derivatives exposure and interconnectedness with major banks.

Regulators thought, maybe we need better risk measurement, transparency, and capital requirements...

You think?

And so, Basel II is born, introducing more sophisticated approaches to measuring and managing credit, operational, and market risk.

How?

Building on Basel I, Basel II introduced three main pillars:

Minimum Capital Requirements: Calculating capital ratios based on risk-weighted assets

Supervisory Review: Enhancing risk management and supervision

Market Discipline: Improving transparency through disclosure

Awesome. All in the clear then, right?

No more LTCM stars to implode? No more systemic banking risks?

Well...

We still have mortgage backed securities and derivatives to be multiplied and rolled up into a globally systemic parlor game.

The bankers and bettors were too fast for the BCBS and Basel, and Basel II was just not fast enough on the draw.

The Great Financial Crisis ensues, and we're right back to square one.

😮 Basel III and the Endgame

Enter Basel III and the Endgame.

In direct response to the Great Financial Crisis of 2008, The BCBS decides to step up its game even more in order to enhance the stability and resilience of the banking sector.

The new new framework introduced several reforms, including changes to capital adequacy requirements, liquidity standards, and leverage ratios.

Aha, there it is!

Leverage Ratios.

So now, in addition to the capital and disclosure requirements of Basel II, banks are now subject to certain ratios they must maintain to stay within the appropriate risk guidelines of Basel.

Liquidity requirements.

The Endgame.

If they step out of line, like John Cleese, they'll be summoned, "Basil!"

One of these key ratios is known as the Supplementary Leverage Ratio (SLR), which measures a bank’s capital against its total leverage exposure.

In other words, the banks must hold a certain amount of liquidity against all its risk assets. And G-SIBs (Globally Systematic Important Banks, aka Too Big To Fail) are held to an even higher standard than regular banks.

And they don't like this one bit.

And so, the big banks and ISDA have written a letter to The Fed and the regulators demanding that this so-called Endgame be re-considered.

And we will get into all of that in the final part of this ISDA and the Endgame newsletter series next week.

Until then, enjoy the rest of your Sunday.

That’s it. I hope you feel a little bit smarter knowing about Basel III and its Endgame and are looking forward to the conclusion of this ISDA Letter series next week.

If you enjoy The Informationist and find it helpful, please share it with someone who you think will love it, too!

Talk soon,

James✌️