Gamma and Short Squeezes

✌️ Welcome to the latest issue of The Informationist, the newsletter that makes you smarter in just a few minutes each week.

🙌 The Informationist takes one current event or complicated concept and simplifies it for you in bullet points and easy to understand text.

🫶 If this email was forwarded to you, then you have awesome friends, click below to join!

👉 And you can always check out the archives to read more of The Informationist.

Today's Bullets:

GME - The Mother of All Short Squeezes

Gammas Made Simple

Mag7 Gamma Time

Inspirational Tweet:

We've all witnessed the meteoric rise of certain stocks over the years, like AMC, GME, and now SMCI. And many attribute the ascents to pump and dump schemes or other market 'manipulations', such as short or 'gamma' squeezes.

Like rocket fuel or a jet blaster ignitions, these dynamics can, in fact, contribute to or even cause the relentless increase in stock prices, at times.

But what exactly are short and gamma squeezes, anyway?

If it all sounds confusing and Greek (pun intended) to you, have no fear. Because we are going to unpack and sort these concepts as easily as you can imagine here, today.

So, grab that cup of coffee and settle in for a Sunday morning ride 'to the moon' with The Informationist.

😱 GME - The Mother of All Short Squeezes

You all remember GameStop (GME) right?

How this company that was supposedly running out of money, borrowing too much, going bankrupt a few years ago?

Yet, instead of the stock going to zero, it shot up like a rocket on a Mars mission, defying gravity, financial expert analysis, and any semblance of reason, really.

But why?

Well first, to understand what happened with GME, you must first know exactly what shorting a stock is, and how short sellers can be squeezed.

See, when you buy and sell a stock, you don't actually take physical possession of that stock. They don't send you a paper certificate like in the good old days of the early New York Stock Exchange, for instance:

Instead, it's just a digital record that is put in your name on a computer, of course. And the brokerage that you bought it through will custody the digital certificate for you (either themself or through their own custodian).

What this enables them to do, is pool all the certificates of a single company that all their customers own together, and allow others to borrow some of the certificates to sell short.

This is called re-hypothecation.

For example:

Peter buys 100 shares of Coca Cola (KO).

Jane thinks KO is garbage and wants to sell it short. And so, she borrows 100 shares of KO through the broker (Peter's shares), and sells it short (she doesn't own it, so she is selling it short) to Mary.

Peter bought, Jane borrowed Peter's shares, and sold them short to Mary.

Now Mary is essentially holding Peter's shares.

This is oversimplified, and there are borrowing fees that Jane pays and some of that is passed through to Peter as short 'rebate', and there are rules around how and when to short, etc., but you get the essence.

Now, what if the stock goes up, high enough that Peter wants to sell?

Well, in this case, the custodian must supply other shares from that big pool of KO shares they have in custody, and let Peter sell them.

Easy, peasy.

Unless, of course, the stock runs so hard, so high, so fast, that many of the original buyers want to sell their shares, outpacing the demand that the custodian can meet for them.

In other words, they lent all the shares out, and now the original buyers want to sell.

What happens?

The broker calls Jane and says, sorry you've lost your borrow. And so, unless you can find additional shares to borrow yourself and give back to us (Peter), then we will be forced to buy your shares back in the open market and close your position.

Likely at a substantial loss.

This is called being bought-in on your borrow.

You can imagine what happens next.

Jane has to buy, likely forcing the stock even higher. Then more original sellers want to sell at the even higher price, and this causes?

Exactly.

More borrowers being bought-in.

Which causes?

The stock to go even higher.

And?

*BOOM*

A short-squeeze.

And this is precisely what happened in GME.

Add the collateral piece that borrowers (short-sellers) must post, and this becomes rocket fuel on the already raging short-squeeze fire.

Because a short seller can theoretically lose an infinite amount of money, the lender requires that borrower to post collateral (cash) to make good on their promise to pay that lender back (give them shares back when they need them).

And so, if the stock rises enough, the borrower must post more collateral (cash).

The vicious cycle repeats, as some of these borrowers fail to post extra collateral, and they are bought in, too.

If this happens at a fast and furious enough pace, it is affectionately known in the hedge fund world as 'getting your face ripped off'.

Precisely what happened in GME.

A short recap for those who have not read the book Dumb Money by Ben Mezrich or seen the movie based on it:

Keith Gill, known on Reddit as "DeepFuckingValue" and on YouTube as "Roaring Kitty" bought about $50K of call options on GME stock in 2019.

Gill, also a CFA, was quite clever, sharing his journey with the investment on r/wallstreetbets, providing updates on his performance, including the good and the bad.

Investors and day traders communicating on r/wallstreetbets believed the company was significantly undervalued.

One reason?

They realized that the custodians had over-lent the shares, to the tune of 140% of the entire float.🤯

And they realized they could manufacture a short squeeze from this. They just had to drive up the price to the point where short sellers would be forced to capitulate and cover their positions at large losses.

Margin call.

One user, Stonksflyingup, even posted a video from the movie Chernobyl, explaining how a short position by hedge fund Melvin Capital could be utilized to trigger a short squeeze, and cause the hedge fund to implode, like a nuclear meltdown.

Which it ultimately did, from the mother of all short squeezes.

In just seven days of trading GameStop traded from $10.65, up to $120.75 (approximately a gain of 1,134%), and back to $22.50, for nearly a full round-trip.

Wheeeee.

Roaring Kitty made about $48 million on the trade.

Super fun for all those involved, except...

the shorts.

Because Melvin Capital went belly up.

Ouch.

🤓 Gammas Made Simple

OK, now that we have short squeezes all sorted out, what about gamma squeezes?

We most often here about gammas in relation to 0DTEs lately, but we will focus on the broader concept here today.

Incidentally, I wrote all about 0DTEs a while ago, and if you're interested, you can find that article in the archives of my Substack, here:

To fully understand gamma, though, we must first review the basics of options. So we will recap that part here.

The options we’re talking about today are simply the right to buy or sell a listed security at a certain price that expires on a certain day.

For example:

If you buy a February 17th $130 Put in AAPL, this would mean you own the right to sell100 shares of AAPL (a single option contract represents 100 shares) at $130, and this right expires on February 17th.

Likewise, if you buy a February 17th $130 Call in AAPL, this would mean you own the right to buy 100 shares of AAPL at $130, and this right expires on February 17th.

A few terms for you today:

Strike Price → this is the price of the security that you are trading the right to buy or sell it at (i.e., $130, in the example above)

Premium → this is the cost of the option itself

Expiry → just as it sounds, this is the day the option expires

Contract → options trade as contracts, and each contract is ‘the right to buy or sell 100 shares worth’ (if I buy 5 February 17th $130 Calls in AAPL, this is 5 contracts, or 500 shares worth)

In the Money → the option is trading at a price that is already profitable for the buyer (if I buy a $120 Call in AAPL and the stock is trading at $130, then the option is $10 in the money)

Out of the Money → just the opposite, this is the amount an option is away from being profitable to the buyer (if I buy a $140 Call in AAPL and the stock is trading at $130, then the option is $10 out of the money)

Simple, right?

And the other side of most options trades is likely a market maker or dealer.

Then, when a dealer sells an option, they have to turn around and protect themselves on the trade.

Here’s how.

Dealers run books of positions using the bank’s money, known as proprietary capital, and hence these dealers are known as prop desks.

The prop desk’s job is to facilitate trades (i.e., take the other side of the customer to make the trade happen) and collect enough fees in commission and premium to make it worthwhile and hopefully cover any losses that are incurred from taking the other side.

They have effectively assumed risk to sell insurance to the buyer of the option—not too different than AIG selling flood insurance to a homeowner in Baton Rouge. Which leaves the dealer exposed to a loss.

And then the dealer has to turn around and hedge that risk themself.

Delta.

See, dealers use a book hedging strategy called delta hedging. An option’s delta estimates how much its value may change with a $1 move in either direction of the underlying security.

So, if the delta of the AAPL $145 Puts in the example above was .53, then for every $1 that AAPL fell in price, the option value would increase by .53c. The delta increases as AAPL price approaches (gravitates to) that $145 level, until it final reaches 1.0. From that point and lower, with every $1 that AAPL drops, the option becomes worth $1 more.

For example, let’s pretend that AAPL’s $145 Puts Delta table looked like:

The dealer might initially delta-hedge the calls in our scenario by shorting 53,000 shares (.53 X 1,000 puts X 100 shares per put). As the price of AAPL rises or falls, the dealer will adjust the the number of shares it is short, accordingly.

If the price moves up to $155, the dealer would cover some of his short until he was short 31,000 shares, and if it moves lower to $149, he would short more to be total short 65,000 shares.

So, if the option buyer was right, or a hedge fund had speculated correctly, and AAPL fell in price as we approach the expiration date, the dealer would be forced to sell more AAPL shares, according to normal risk management policies.

The further AAPL falls, the more the dealer must sell.

All the way until $145, where he has to be short the entire position to cover himself.

In other words, as the price gravitates to that option strike price of $145, the selling pressure increases dramatically, only pushing the delta even higher.

This is known as gamma, or the rate of change of the rate of change (delta) of an option.

And so, gamma is actually the delta of the delta.

And it works on both sides: stocks can gravitate lower to put strikes and higher to call strike. Dealers will buy and sell accordingly, often causing the very momentum they are hedging against. Traders recognize this, and a pile-on occurs, accelerating themove.

And that, my friends, is a gamma squeeze.

The rate of change of the delta accelerates.

And so, now you can see why it makes sense that gamma is highest when an option is at the money and is at its lowest when it is further away from the money.

Gamma is also highest for options closer to expiration than ones further out, typically.

😵💫 Mag7 Gamma Time

Where have we seen some gamma squeezes lately?

In the Mag7 stocks, and tech-related companies, of course.

As we just learned, a gamma squeeze is self-reinforcing, in that when investors buy call options in a stock, it causes market makers to hedge their own short calls by buying the stocks themselves, hence driving up the stock prices.

Some investors mistake this price movement as fundamentally bullish when in reality, it can sometimes be the result of excessive speculation instead.

Or purposeful attempts to engineer a squeeze, a la r/wallstreetbets.

However, once the call option's volatility is too high, or the options expire, this can cause the stock to plummet.

Take a peek at the charts of some these stocks on expiration days of recent months, and you will see what I mean. When a stock has an unusually large number of options expiring on a day, it can be something of a self-fulfilling prophecy.

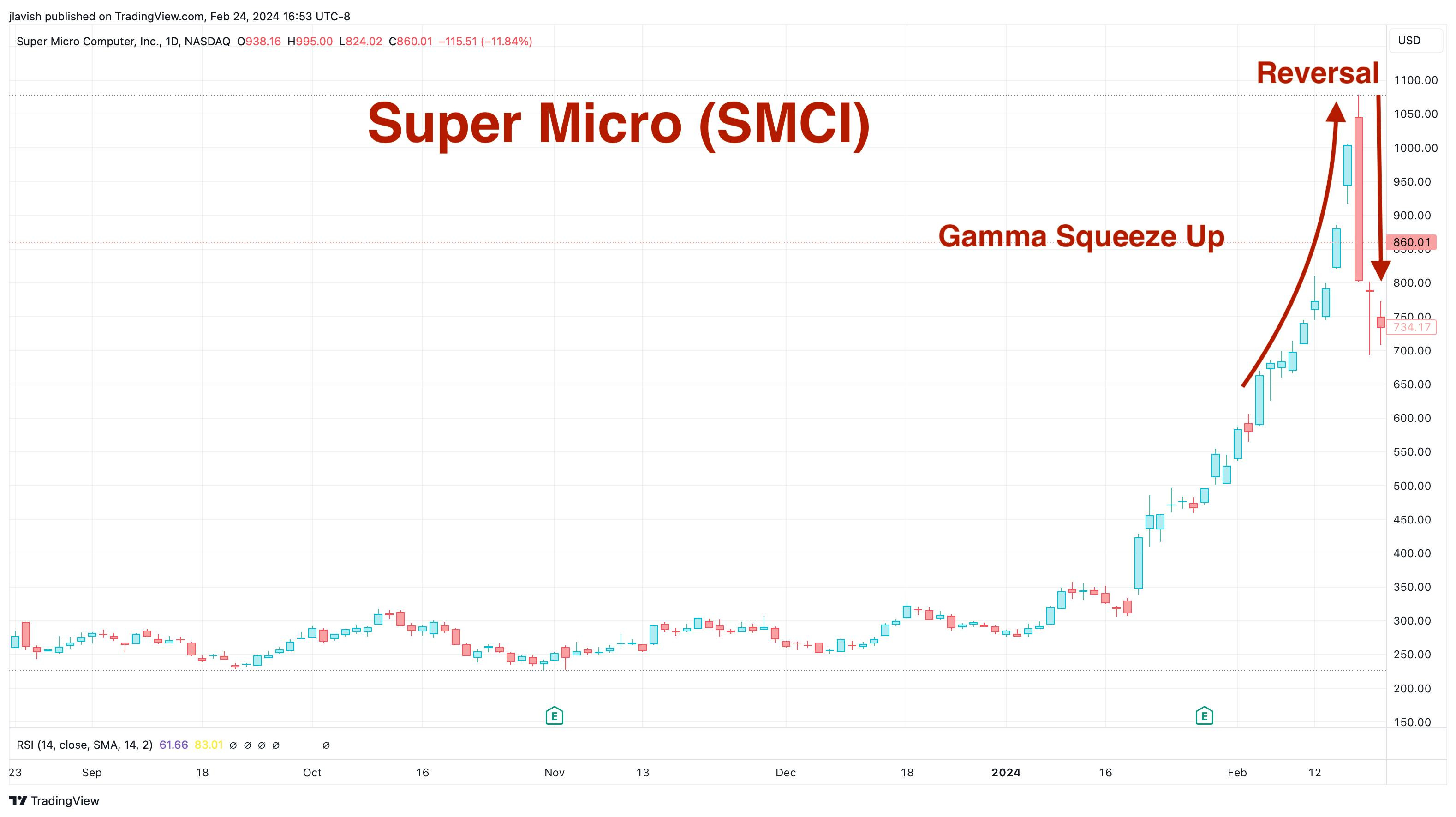

Here's a recent gamma squeeze in Super Micro Computer, Inc (SMCI)...

The options activity:

And the resulting stock reaction and activity:

The journey back to earth (the reversal) can be swift and painful.

Now, to be clear, this type of activity and near-euphoria can go on for a long time, or to extreme levels, as we learned in GME and other squeezes.

But it is something to keep in mind when observing these trading patterns and extraordinary price movements during in short periods.

Especially with the newly-minted Magnificent 7, and their cousins.

If you are aware of this, it may help you understand seemingly erratic movements and prepare you for how to profit on, or avoid taking losses from, these moves.

Because in the end, we would all rather be on the side of Roaring Kitty than Melvin Capital.

That’s it. I hope you feel a little bit smarter knowing about short and gamma squeezes and are ready to start incorporating this knowledge into your own trading and investing process.

If you enjoyed this newsletter and found it helpful, please share it with someone who you think will love it, too!

Talk soon,

James✌️