ISDA and its Endgame - Part 3

✌️ Welcome to the latest issue of The Informationist, the newsletter that makes you smarter in just a few minutes each week.

🙌 The Informationist takes one current event or complicated concept and simplifies it for you in bullet points and easy to understand text.

🫶 If this email was forwarded to you, then you have awesome friends, click below to join!

👉 And you can always check out the archives to read more of The Informationist.

Today's Bullets:

ISDA and Basel

The Ratios

The Real Endgame

Inspirational Tweet:

Welcome to Part 3 of the ISDA and its Endgame series, where we have been working up to answering the question:

Who is ISDA, what's the SLR, and why the heck should we care?

While this all may sound super foreign or confusing or even, dare I say, boring, the truth is that it matters a whole lot more than you may think.

Or if you've been reading along, you now suspect that it really is a BFD.

And so, in this final part of the series, let's get to the answer we've been looking for, but let's keep it nice and simple as always, shall we?

So grab a cup of coffee and settle into your favorite seat for this Sunday's issue of The Informationist.

🤨 ISDA and Basel

For the readers who have been following along the last few weeks, you now know exactly what (or rather, who) ISDA is and its background.

If you have not yet seen Parts 1 and 2 of this series, you can find them here:

and here:

For the TL;DR crowd, and as a quick review for everyone, in Part 1, we covered ISDA.

Specifically, we learned that the International Swaps and Derivatives Association (ISDA) was created to add structure and standards to the global swaps and derivatives market that now has a notional value of over $1 quadrillion.

Big business.

And as for the who part of ISDA, its primary managers are former and current Wall Street and colossal Main Street firms'...

Bankers.

One important note: the vast majority of these directors, executives, and managers all still work at these banks while they hold their positions at ISDA.

As for Part 2, we looked into the Basel accords and their introduction.

Here we learned that the Basel Committee on Banking Supervision (BCBS) was founded after a key German bank collapse, back in 1974. BCBS members are basically the central bankers and regulators from the G10 countries

A few key points of the Basel accords:

Under Basel I, bank assets were classified according to their level of risk

Banks were required to maintain emergency capital based on that classification

The capital requirement was set at 8% of risk-weighted assets (RWAs)

Basel II introduced three main pillars:

Minimum Capital Requirements: Calculating capital ratios based on risk-weighted assets

Supervisory Review: Enhancing risk management and supervision

Market Discipline: Improving transparency through disclosures

Finally, under Basel III, banks were introduced to new and important Leverage Ratios.

The Basel III Endgame.

Visually:

And so, recently, the big banks and ISDA have written a letter to The Fed and the regulators (The ISDA Letter) demanding that this so-called Basel III Endgame be re-considered.

What's the big deal, you may be asking.

What's to re-consider, and why are the banks making a fuss about these new ratios?

Yeah, about that...

😵💫 The Ratios

Let's keep this simple, high level.

You may recall that in April 2020, after the markets had drawn down and Treasury markets became dysfunctional, the Fed decided to reduce bank reserve requirements to zero across all deposit tiers.

This was to provide additional liquidity to banks and hence the Treasury auctions amid the disrupted markets.

One of the key reasons the Fed was 'able' to do this was the recently implemented Basel III ratios that required banks to hold a certain amount of reserves above and beyond the amount of 'risk assets' on their balance sheets.

A note:

There are basically three different classifications of banks.

We have Global Systemically Important Banks (G-SIBs), which are the 'Too Big To Fail' banks, like JP Morgan, Citigroup, and Morgan Stanley here in the US. G-SIBs face the most stringent requirements in the ratios listed below.

Then there are Domestic Systemically Important Banks (D-SIBs), smaller and important to a country's domestic financial system but not necessarily to the global system, like G-SIBs. Examples of D-SIBs would be American Express and Capital One Financial.

Then there are all the other banks, which generally follow Basel III standards, but with much less intense supervisory scrutiny. Think: Regional Banks and Community Banks.

The Ratios:

Liquidity Coverage Ratio (LCR):

The LCR covers short-term liquidity risk

Banks must hold enough high-quality liquid assets (HQLA) to cover potential cash outflows during a 30-day stress scenario (you all recall the Silicon banking debacle from a year ago? Yeah, they failed this one...)

Net Stable Funding Ratio (NSFR):

The NSFR measures the stability of a bank’s funding sources relative to its activities over the long term (i.e., cash on hand vs. loan obligations)

By encouraging stable, longer-term funding, the NSFR reduces reliance on volatile short-term funding markets (30-year US Treasuries have been quite volatile, for instance, as SVB learned the hard way, and so they pretty much failed this one, too)

Supplementary Leverage Ratio (SLR):

The SLR focuses on preventing excessive leverage (Oh, SVB)

It requires banks to maintain a minimum capital buffer relative to their total exposure (both on- and off-balance sheet)

Unlike risk-weighted ratios, the SLR treats all assets equally, regardless of their riskiness

Ah, this last ratio is quite important today, as this is the one that the ISDA Letter seeks to address.

Essentially, the SLR is meant to prevent banks from becoming over leveraged.

And this is exactly the ratio, the letter from ISDA to the Fed and other agencies seeks to change.

The Letter:

I encourage you to have a read on this, but I'll give you the broad streaks and the main highlight here.

Because the next paragraph reads like this:

In the 'did I just read what I think I read?' category'...

You, in fact, did.

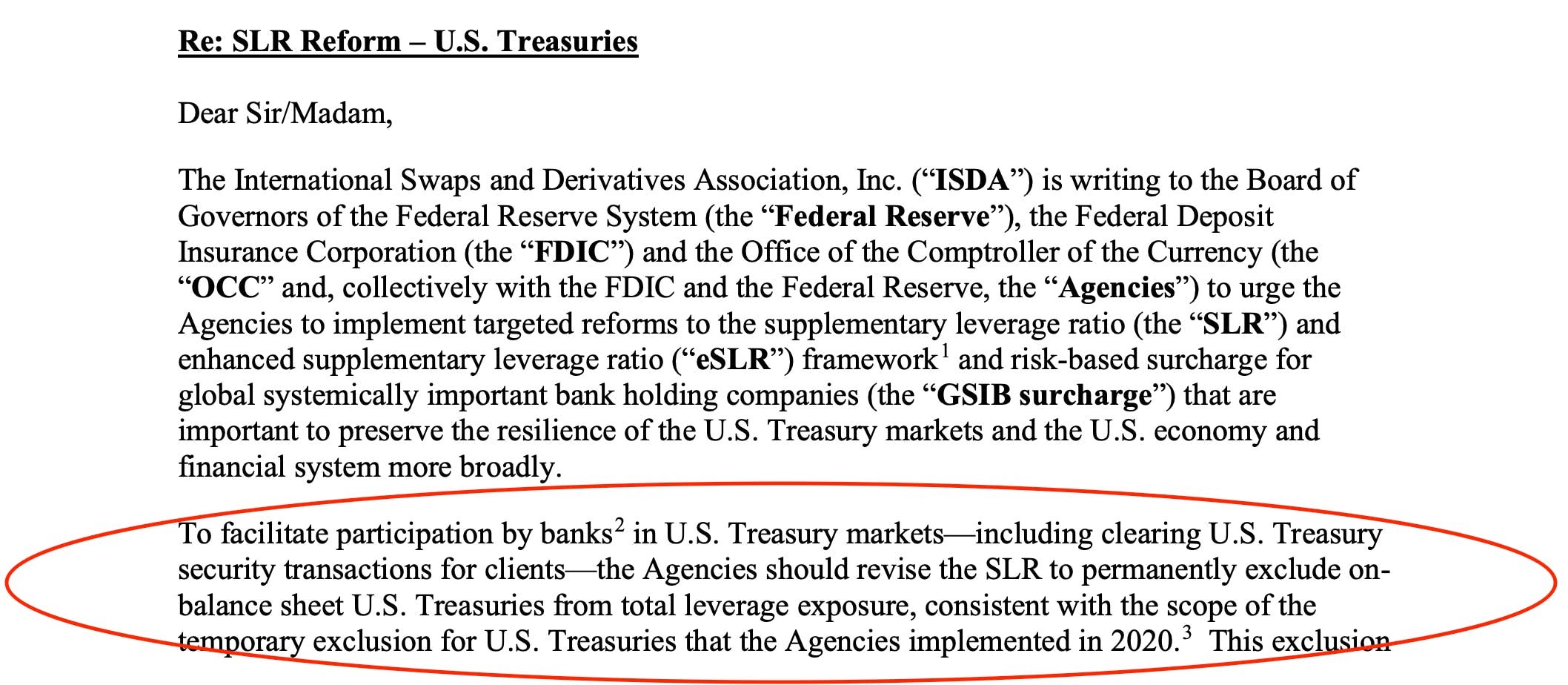

ISDA, and thereby the banks who manage and oversee the association, are seeking to permanently exclude US Treasuries from risk and leverage exposure ratios.

Say what?

🫣 The Real Endgame

I mean, we've been told for decades and decades that US Treasuries are risk-free.

Or are they?

Back to the Silicon Valley Bank debacle.

You may recall how that bank had a problem because it held US Treasuries in reserve, and these USTs fell in value because of the rise in interest rates.

If you don't recall, or never knew that and are interested in re-visiting that banking horror show, I wrote all about it in an Informationist newsletter right after it happened.

You can find that in the Informationist Substack archives, here:

TL;DR: SVB held lots and lots of USTs (but not enough), and when interest rates rose, the value of these USTs fell, especially the long-duration (think 10yr to 30yr Treasuries).

Problem is, SVB didn't hedge against interest rate risk.

Oops.

Bad practices.

But this is a simple demonstration of how US Treasuries are anything but risk-free.

They are marketable securities that move in price according to supply and demand and the current rate environment.

Bottom line: the ISDA Letter seeks to reclassify US Treasuries from risk assets to risk-freeassets.

what?

That's right. The banks are seeking to have US Treasuries removed entirely from the risk-asset side of the SLR ratio.

Their argument?

"...to preserve the resilience of the U.S. Treasury markets and the U.S. economy and financial system."

They are basically petitioning to remove them from the calculations, permanently.

See, when we went into Covid lockdown, the stock and bond and even US Treasury markets became dysfunctional for weeks. As you likely well know. The Fed's response included massive money printing, buying US Treasuries, and removing reserve requirements.

They also removed US Treasuries from the SLR calculations for a couple of years.

Uh oh.

The Fed opened the door.

And now the Big Bad Bank Camel's head is in the regulatory tent.

But what will the Fed do?

After all, with the US government running multi-trillion dollar deficits, the US Treasury has little choice but to keep borrowing more money to fund those deficits.

They need to keep issuing more and more debt.

More Treasuries.

(to the moon)

The banks argument is that they need room on their balance sheets to own all those Treasuries. They can't be restrained by these onerous risk ratios. The Treasury and its market needs the banks.

They need the banks to be able to buy MOAR.

And so, while it remains unclear what the Fed's decision is on this matter, and whether they, along with the other agencies, will, in fact, change the ratios and classifications of US Treasures to appease the banks.

Or should I say, to appease the US Treasury?

After all, what could possibly go wrong there?

Well. Endgame, indeed.

That’s it. I hope you feel a little bit smarter knowing about ISDA, Basel, and the Endgame Letter. If you enjoy The Informationist and find it helpful, please share it with someone who you think will love it, too!

Talk soon,

James✌️